Key Takeaways:

If you're a Muslim professional already investing through Vanguard, Fidelity, or Schwab, you've probably had the same quiet concern: your S&P 500 index fund includes alcohol producers, conventional banks, and gambling companies. You're building wealth - but not entirely on your terms.

The question most people then ask is a reasonable one: if I switch to Shariah Compliant investing, am I giving up returns to stay compliant?

This article gives you a clear, honest comparison - what the two approaches actually look like structurally, where they differ in practice, and what the performance conversation really involves for a long-term U.S. investor.

What Is Conventional Investing?

Conventional investing is the standard approach to building wealth through financial markets in the U.S. It involves no restrictions on the types of assets or industries you can invest in - the only criteria are financial: expected returns, risk tolerance, and time horizon.

In practice, conventional investing in the U.S. stock market typically looks like this:

Stocks/equities market investing either by buying individual stocks or through broad index funds (S&P 500, total market funds) that include any publicly traded company regardless of industry or business model. A standard S&P 500 index fund includes banks, alcohol companies, casinos, tobacco companies, weapons manufacturers, and conventional insurance - alongside technology, healthcare, and consumer goods companies.

ETFs and mutual funds that bundle stocks and bonds into diversified portfolios. Most target-date retirement funds, for example, hold a mix of equities and bonds - with bond allocations increasing as the investor ages.

Interest-based financial instruments including corporate bonds, government bonds, and money market funds, all of which generate returns through fixed interest payments.

Conventional investing dominates the U.S. market for straightforward reasons: it's accessible, low-cost (particularly through passive index funds), and has delivered consistent long-term returns for investors who stayed invested through market cycles.

What Is Shariah Compliant Investing?

Shariah-compliant or Islamic investing - applies an ethical and religious framework to investment decisions, rooted in the principles of Islamic finance.

The goal is identical to conventional investing: build wealth over time through productive economic activity. The difference is that certain mechanisms and industries are excluded based on Islamic principles.

The three core rules of halal investing:

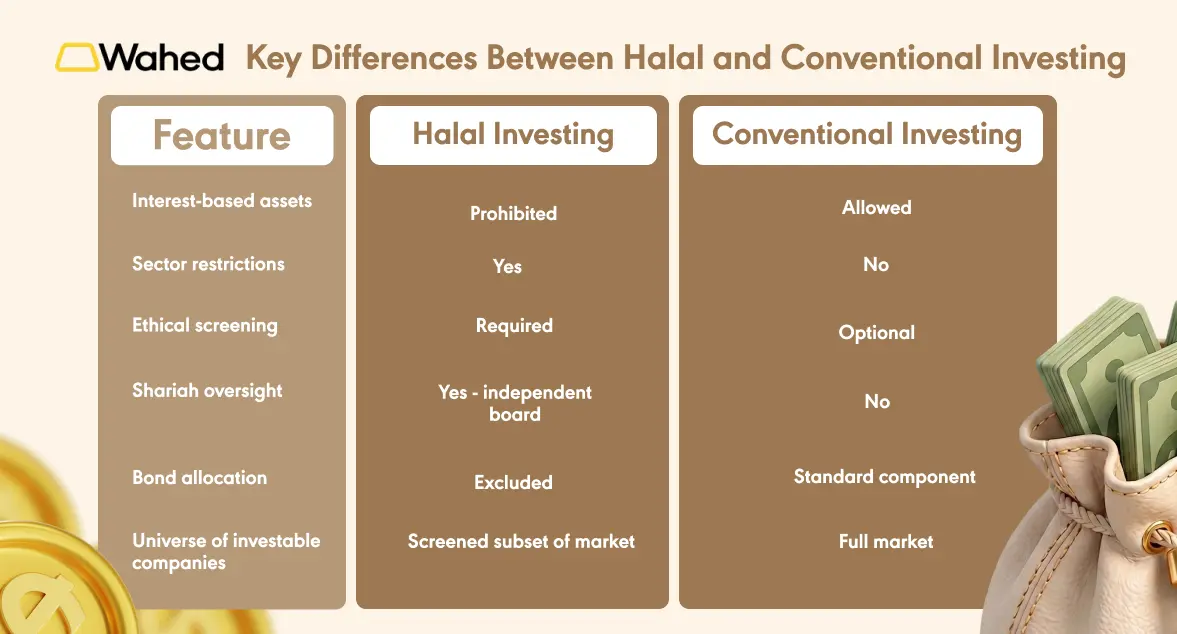

Avoid riba (interest). Any financial return generated through lending at interest is prohibited. This is the most significant structural difference from conventional investing - it categorically excludes bonds, conventional savings instruments, and most fixed-income products. To be direct: Conventional bonds are not Shariah Compliant. Whether government, corporate, or municipal, bonds generate returns through interest payments, which constitute riba.

Avoid haram industries. Companies whose primary business involves prohibited activities cannot be held in a Shariah Compliant portfolio, regardless of their financial performance.

Invest in ethical businesses. Beyond exclusions, Shariah Compliant investing favours companies engaged in productive, society-contributing activities - genuine business operations rather than financial speculation or harmful products.

Key Differences Between Shariah Compliant and Conventional Investing

The most consequential difference for U.S. investors is the bond exclusion. Standard retirement advice - including target-date funds and traditional portfolio construction - relies heavily on bonds for stability and income generation, particularly as investors age. A Shariah Compliant portfolio replaces this with a different risk management approach, typically through equity diversification across sectors and geographies rather than asset class diversification.

Industries Avoided in Shariah Compliant Investing

The sector exclusions in Shariah Compliant investing are often misunderstood as arbitrary. Each reflects a consistent principle about harm, exploitation, or impermissibility under Islamic ethics.

Alcohol: The production, distribution, and sale of alcohol is prohibited, making companies like Anheuser-Busch, Diageo, and major grocery retailers with significant alcohol revenue non-compliant.

Gambling: Casinos, online gambling platforms, sports betting companies, and lottery operators are excluded. The prohibition stems from the concept of maysir - acquiring wealth through chance rather than productive effort.

Conventional banking: Traditional banks operate on interest-based models - taking deposits at one rate and lending at a higher rate. This riba-based business model makes them non-compliant, which means major institutions like JPMorgan, Bank of America, and Wells Fargo are excluded from portfolios.

Weapons and defence: Companies whose primary revenue comes from weapons manufacturing are excluded, particularly those involved in weapons systems used in conflicts affecting civilian populations.

Adult entertainment: Entirely excluded under Islamic ethics regarding modesty and human dignity.

Tobacco: Excluded on the grounds of harm - a principle increasingly aligned with ESG (Environmental, Social, Governance) frameworks in conventional finance as well.

The rationale across all categories is consistent: Shariah Compliant investing refuses to profit from industries that generate wealth through harm, exploitation, or ethical violation. This is a values-based constraint, not a financially arbitrary one.

How Shariah Compliant Investment Screening Works

Identifying which companies pass Shariah screening involves two distinct layers, typically overseen by an independent Shariah supervisory board:

Business activity screening is the first filter. It identifies and eliminates companies in prohibited sectors - the industries listed above. Any company deriving more than 5% of its total revenue from non-compliant activities is typically excluded, even if its primary business is otherwise permissible.

Financial ratio screening is the second layer. Even companies in permissible industries can fail if their financial structure relies too heavily on interest-based debt or generates significant interest income. These thresholds may vary depending on different Shariah screening methodologies and interpretations across scholars and screening providers, but generally include:

- Interest-bearing debt below around 33% - 35% of total assets or market capitalisation

- Non-compliant income below 5% of total revenue

- Accounts receivable below 49% of total assets (to avoid excessive money-lending characteristics)

Companies that pass both layers are considered Shariah-compliant. Shariah scholars Islamic finance experts with both religious and financial training - sit on advisory boards that validate screening methodologies, review fund holdings periodically, and issue guidance when edge cases arise. This oversight layer is what distinguishes a genuinely Shariah-compliant product from a self-described "ethical" fund without accountability.

Does Shariah Compliant Investing Perform Differently?

This is the question most Muslim professionals are actually asking - and it deserves a straight answer rather than vague reassurance.

The honest position: Shariah Compliant investing performs differently, not necessarily worse. Understanding why requires looking at what the exclusions actually do to a portfolio.

Sector bias toward technology and healthcare. Because conventional banking, alcohol, and tobacco are excluded, halal equity portfolios tend to be overweight in technology, healthcare, and consumer goods - the sectors that remain after screening. Over the past decade, this has generally not been a disadvantage; technology in particular has significantly outperformed broader market averages.

Bond exclusion removes fixed income drag. In conventional portfolio theory, bonds are supposed to reduce volatility and provide stable income. The trade-off is lower long-term returns, since equities historically outperform bonds over extended periods. A Shariah Compliant portfolio that is fully invested in equities does not have this drag - which can be an advantage over long time horizons, while meaning more short-term volatility than a balanced conventional portfolio.

Diversification is narrower by universe but not necessarily by outcome. A screened equity universe is smaller than the full market, but a well-constructed portfolio across multiple geographies, market caps, and sectors can still achieve meaningful diversification. The correlation of Shariah Compliant equity returns with global equity indices has historically been close - not identical, but not dramatically divergent.

What to avoid: any source claiming Shariah Compliant investing definitively outperforms or underperforms conventional investing. Both claims are misleading. Performance depends on time period, market conditions, portfolio construction, and the specific benchmark you're comparing against. The reasonable expectation is competitive long-term performance, not guaranteed superiority.

Example: Shariah Compliant Portfolio vs Conventional Portfolio

To make the structural differences concrete, consider two simplified portfolios for a U.S. Muslim professional investing $100,000 for long-term retirement:

Conventional Portfolio (S&P 500 index fund + bonds):

Sector exposure includes: financials (~13%), healthcare (~13%), technology (~28%), energy (~4%), consumer staples including alcohol (~7%), bonds generating interest income throughout.

Shariah Compliant Equity Portfolio:

Sector exposure: technology (~35%), healthcare (~18%), industrials (~15%), consumer goods (~12%), materials and energy (~10%), zero conventional banking, zero bonds.

The two portfolios look different - primarily in the absence of financials and bonds, and the higher technology concentration in the halal version. Over long time horizons, both have generated meaningful wealth for investors. The Shariah Compliant portfolio carries more equity concentration risk but avoids the interest income embedded throughout the conventional structure.

Who Should Consider Shariah Compliant Investing?

Muslims seeking faith-aligned investing are the primary audience - those who want their financial behaviour to reflect their values without accepting a financial penalty for doing so.

Ethically-motivated investors more broadly. The exclusions in Shariah Compliance investing overlap substantially with ESG investment criteria. Alcohol, weapons, gambling, and tobacco exclusions appear in many socially responsible investment frameworks. Some non-Muslim investors choose Shariah Compliant funds precisely because of their ethical screening rigour and independent oversight.

Long-term investors. The equity-heavy nature of Shariah Compliant portfolios (given the bond exclusion) makes them particularly suited to investors with long time horizons - those in their 20s through 40s who have decades for compounding to work. The short-term volatility of an equity-heavy portfolio becomes less meaningful over a 20–30 year investment horizon.

Building Wealth the Islamic Way

For Muslim professionals already investing through conventional platforms, the question is no longer whether Shariah Compliant investing is viable - it is. The question is whether your current portfolio reflects your values, and whether you're willing to align the two.

Values-based investing does not require accepting financial sacrifice. It requires finding the right vehicle - one built with Islamic finance principles at its foundation, not retrofitted as an afterthought.

Disclosure:

This article is for educational purposes only and does not constitute religious, financial, or legal advice. Investing involves risk, including the loss of principal. This is not a recommendation to buy or sell any specific security. We recommend consulting a qualified Islamic scholar for guidance on your specific situation. Past performance is not indicative of future results. Wahed Invest LLC is a registered investment adviser with the SEC.