Key Takeaways:

If you're a Muslim professional in the U.S. already thinking about retirement savings, you've likely faced a decision that most financial content doesn't address properly: not just which IRA to open, but whether either one can be made Shariah-compliant - and if so, which structure actually serves you better given your income and career stage.

The short answers: both Roth & Traditional IRAs can be halal, but which one is better depends almost entirely on where you are in your income trajectory. This article gives you the framework to decide.

Understanding IRAs: A Quick Overview

An Individual Retirement Account (IRA) is a tax-advantaged investment account available to any American with earned income. Unlike a 401(k), which is tied to your employer, an IRA is opened independently - through a brokerage, a bank, or an investment platform - and you control everything about it, including what goes inside.

That control is the key detail for Muslim investors.

The U.S. government uses IRAs to incentivize long-term retirement savings by offering tax benefits that standard brokerage accounts don't get. The two main types - Traditional and Roth - differ in when those tax benefits apply. Both have a 2026 annual contribution limit¹ of $7,500 (or $8,600 if you're 50 or older).

What Is a Traditional IRA?

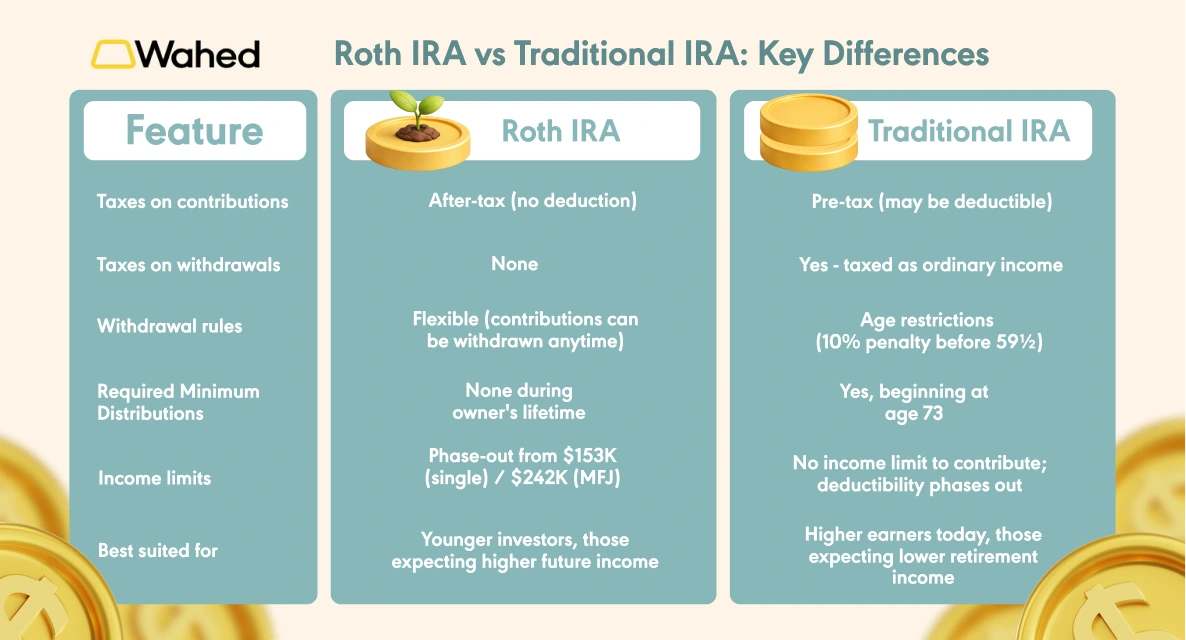

A Traditional IRA lets you contribute money before it's taxed - reducing your taxable income in the year you contribute. The money then grows tax-deferred inside the account, and you pay income tax when you withdraw it in retirement.

How it works:

- Contributions: Pre-tax (may be tax-deductible depending on income and workplace plan)

- Growth: Tax-deferred - no annual capital gains or dividend tax

- Withdrawals: Taxed as ordinary income

- Required Minimum Distributions (RMDs)²: Must begin at age 73

Example scenario: A Muslim engineer earning $110,000 contributes $7,500 to a Traditional IRA. If she's not covered by a workplace retirement plan, that $7,500 reduces her taxable income to $102,500 - saving her roughly $1,650 in federal taxes at the 22% bracket this year. The trade-off: when she withdraws that money in retirement, she'll pay tax on it at whatever rate applies then.

For Traditional IRA deductibility in 2026³, the phase-out range for those covered by a workplace plan is $81,000–$91,000 for single filers and $129,000–$149,000 for married filing jointly. Above those thresholds, contributions are still allowed - they're just not tax-deductible.

What Is a Roth IRA?

A Roth IRA works in reverse. You contribute money that has already been taxed, and in exchange, everything inside the account - contributions and all growth - comes out completely tax-free in retirement.

How it works:

- Contributions: Post-tax

- Growth: Tax-free - compounds without any future tax liability

- Withdrawals: Entirely tax-free after age 59½ (with 5-year holding period met)

- RMDs: None - you're never forced to draw down the account

Example scenario: A Muslim tech professional earning $85,000 contributes $7,500 to a Roth IRA. He pays tax on that $7,500 now at his current 22% rate. But 30 years from now, if that $7,500 has grown to $57,000 inside a halal equity portfolio at 7% annual return, he withdraws every dollar of it without paying a cent in tax. The growth - roughly $49,500* - is completely his, free and clear.

Roth IRA income limits in 2026⁴: the contribution phase-out begins at $153,000 for single filers and $242,000 for married filing jointly, with full phase-out at $168,000 and $252,000 respectively.

Roth IRA vs Traditional IRA: Key Differences

Are IRAs Halal for Muslims?

This is the question that stops many Muslim investors from opening either type of account - and the answer requires clarity rather than caution.

The IRA account structure itself is neutral under Shariah. It is a legal wrapper - a container governed by U.S. tax law. There is no interest mechanism built into the IRA itself. The government is not lending you money, and you are not lending it. The tax benefit is a government incentive, not riba.

What determines halal or haram status is entirely what you invest in inside the account.

Three principles govern that:

Avoiding riba: Interest-bearing instruments - bonds, conventional savings vehicles, money market funds - generate returns through interest and must be avoided. This means a standard "balanced" or "target-date" fund, which typically holds 30-40% bonds, is not Shariah-compliant.

Avoiding haram industries: Conventional banks, alcohol companies, gambling businesses, tobacco, weapons manufacturers, and adult entertainment are impermissible regardless of their financial performance. This rules out most standard S&P 500 index funds, which include all of these.

Shariah screening: Even within permissible industries, companies must pass financial ratio tests - typically, interest-bearing debt below 33% of total assets and non-compliant income below 5% of total revenue. Pre-screened Shariah-compliant ETFs and managed portfolios handle this automatically. Thresholds may vary depending on different Shariah screening methodologies and interpretations across scholars and screening providers.

The practical conclusion: a Roth IRA or Traditional IRA filled with Shariah-compliant investments is entirely halal. A Roth IRA filled with a conventional Vanguard target-date fund is not.

Which IRA Is Better for Muslims?

The Roth vs Traditional decision is fundamentally a tax timing question: do you pay tax now, or later? And the right answer depends on where you expect your income - and therefore your tax rate - to be over your lifetime.

Here's the framework:

The Roth IRA Is Likely Better If You Are:

A younger investor (25–35) whose income is still growing. You're probably in the 22% or lower bracket today. Paying tax now at 22% to enjoy tax-free growth for 30+ years is almost always the better deal.

Expecting significantly higher income later. Engineers, doctors, finance professionals, and consultants often see income grow substantially over their career. Locking in a lower tax rate today by choosing Roth means future growth - potentially over a much higher tax bracket - escapes taxation entirely.

Prioritizing flexibility. Roth contributions (not earnings) can be withdrawn at any time without penalty. This makes the Roth IRA function partly as an accessible emergency reserve alongside a retirement vehicle - something that appeals to first-time investors who want flexibility before they're fully committed to locking money away.

Planning for estate transfer. The Roth IRA has no RMDs during the owner's lifetime, meaning you can leave the account to grow indefinitely and pass it to heirs - making it a powerful tool for intergenerational wealth, which aligns strongly with Islamic values around legacy and family.

The Traditional IRA Is Likely Better If You Are:

A high earner today - particularly if you're above $150,000 as a single filer or above $200,000 as a married couple - and expect to be in a meaningfully lower tax bracket in retirement. The upfront deduction delivers real savings today.

Looking to reduce taxable income this year. If you're in the 32% or 35% bracket and eligible to deduct Traditional IRA contributions (i.e., not covered by a workplace plan, or within the deductible income range), the immediate tax saving is substantial.

A small business owner with variable income. In a low-income year, a Roth may make sense. In a high-income year, a Traditional IRA contribution can reduce the tax bill meaningfully.

What If Your Income Is Above Roth Limits?

For Muslim professionals earning above $168,000 (single) or $252,000 (married filing jointly) in 2026, direct Roth IRA contributions are not permitted. However, there is a widely used strategy called the backdoor Roth IRA: you contribute to a non-deductible Traditional IRA and then convert it to a Roth. When structured correctly, this is a legitimate way for higher earners to access Roth benefits - and it remains compatible with halal investing provided the underlying investments are Shariah-compliant.

If you're considering this, consult a tax professional, as the pro-rata rule may apply depending on other Traditional IRA balances you hold.

How Muslims Can Invest in IRAs the Halal Way

Whichever IRA structure you choose, the investment approach inside the account is the same. There are three practical options:

1. Shariah-Compliant ETFs: Pre-screened funds that track halal equity markets, removing the need to vet individual companies. Low cost, beginner-accessible, and overseen by Shariah advisory boards. The most straightforward starting point for most investors.

2. Halal Stock Portfolios: A self-directed approach where you select individual Shariah-screened companies - typically in technology, healthcare, and consumer goods. Requires more research but gives full transparency over what you own.

3. Managed Halal Investment Portfolios: A professionally built and rebalanced halal portfolio matched to your risk tolerance. You answer a few questions; a Shariah-compliant allocation is constructed and maintained for you. The right fit for busy professionals who want compliance without the ongoing workload.

Example: Halal Retirement Investing With an IRA

Let's make the numbers concrete.

A Muslim professional contributes the 2026 maximum of $7,500 per year into a halal equity portfolio - either Roth or Traditional - starting at age 30, with a consistent hypothetical 7% annualised return*.

After 30 years:

The difference - roughly $156,000 - represents the tax paid at withdrawal on a Traditional IRA, assuming a 22% retirement tax rate. If that rate is higher (say 28–32%, which is plausible for a high earner), the Roth advantage widens further.

The key insight: the investment growth inside both accounts is identical. The only variable is when and how much of it the government takes. Choosing correctly based on your income profile today is how you keep as much of that growth as possible.

The above example does not include variables regarding the difference of pre-post tax deductible contributions.

Build a Halal Retirement Portfolio That Fits Your Tax Strategy

The Roth vs Traditional question matters - but the more important question is whether your retirement account is actually working for you in a Shariah-compliant way. Many Muslim professionals discover their IRA holds conventional index funds, bonds, or banking stocks they were never aware of.

Try our retirement calculator.

Sources:

¹ Internal Revenue Service (2025), “Retirement Topics – IRA Contribution Limits,” https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

² Internal Revenue Service (2025), “Retirement Topics – IRA Contribution Limits,” https://www.irs.gov/retirement-plans/plan-participant-employee/retirement-topics-ira-contribution-limits

³ Forbes (2026), “Tax Breaks: The Slow Down, Double Check Edition,” https://www.forbes.com/sites/tax-breaks/2026/02/28/tax-breaks-the-slow-down-double-check-edition/

⁴ TIAA (2025), “IRA Contributions: Income and Deduction Limits,” https://www.tiaa.org/public/retire/financial-products/iras/ira-contributions-tax-benefits/income-and-deduction-limits

Disclaimer:

* For illustrative purposes only and is not intended to represent results of a real investment. 7% hypothetical return shown is based on historical averages. Rates of return vary of time.

This article is for general and educational purposes only and does not constitute financial or investment or tax advice. Tax rules and contribution limits are subject to change. Consult a qualified tax advisor regarding your specific situation. Investment involves risk, including loss of principal. Past performance is not indicative of future results. Wahed Invest LLC is a registered investment adviser with the SEC. The term halal denotes that permissibility in accordance with Islamic law. Wahed Invest does not provide tax advice.

Wahed Invest does not provide tax advice and this should not be considered tax advice. Tax laws and regulations are subject to change. When taking withdrawals from an IRA before age 59½, you may have to pay ordinary income tax plus a 10% federal penalty tax. Withdrawals from a Roth IRA are tax-free if you are over age 59½ and have held the account for at least five years; withdrawals taken prior to age 59½ or five years may be subject to ordinary income tax or a 10% federal penalty tax, or both. Consult a tax professional regarding your specific situation.