.jpeg)

Key Takeaways:

How to Start Investing in Halal Real Estate With $5,000

Most people assume real estate investing starts with a mortgage. For Muslim investors in the U.S., that assumption runs into a problem before anything else: conventional mortgages charge interest, and interest based debt is not permissible under Islamic law.

The assumption worth questioning is that is owning property and investing in real estate the same thing? Simply put, they’re not. You can have exposure to real estate without holding title to a property. And at $5,000, there are some structures that make it possible.

This article covers four structures that are available to Muslim investors in the U.S. at this capital level: what each structure is, how it works and the Shariah questions each one raises. Please note that mentioning an option here is not an endorsement of it. Every investment requires independent due diligence.

What Makes a Real Estate Investment Shariah-Compliant?

Three things are worth understanding before looking at any specific option.

Interest based debt in the structure: The concern is not only about mortgages you personally take out. It extends to any debt at the asset level, the fund level or built into how returns are structured. If borrowed money is earning interest anywhere in the chain, that raises a Shariah issue regardless of how the product is marketed.

Where the rental income comes from: Rental income from tenants using a property for lawful purposes is permissible. Rental income from tenants in industries like alcohol or gambling is not. This is an asset level question and it requires ongoing attention. A property that passes a Shariah screen at acquisition can fail it later if the tenant changes.

Who reviewed it: A product that calls itself Shariah-compliant without independent scholarly oversight is in a different category from one that has been reviewed and certified by qualified scholars. The governance structure is important.

These three questions apply to every option below: is there debt in the structure, where does the income come from and who actually checked it.

Can You Start Investing in Halal Real Estate With $5,000?

Not if the goal is buying a house outright. The national median home price in the U.S. is $403,2001 as of early 2026. Purchasing with cash and no debt is the cleanest Shariah structure for direct property ownership. At $5,000, that’s not on the table.

What $5,000 does open up is a different category of structure. Pooled capital arrangements, fractional ownership platforms, and managed real estate funds can be accessed at this level, and some considerably below it. These are not the same as owning a property. The risk profile is different, the Shariah questions are different, and the level of control you have is different.

Here is what each one involves.

Option 1: Pooled Real Estate Investment Structures

Pooled real estate investing means a group of investors combine capital to access property together. The pooled funds are used to acquire assets and returns are distributed among participants according to their share of the contribution.

Within Muslim communities in the U.S., this often takes an informal shape. A group of family members, friends, or community members pool savings to purchase a property collectively, splitting the rental income and any eventual sale proceeds according to each person's contribution. No platform, no intermediary, no minimum ticket size. Just a group of people who trust each other and a shared asset.

From a Shariah perspective, the concept is well-established. Musharakah, a partnership structure where multiple parties contribute capital and share in profits and losses proportionally, is one of the foundational contracts in Islamic finance. When it is structured cleanly, this kind of arrangement can be among the more naturally permissible approaches to property investing.

What to watch for Shariah compliance: The challenge is that informal structures are, by definition, informal. There is typically no regulated oversight, no standardized documentation and no formal investor protections in place. What happens if one party wants to exit? What are the rights of each investor if the property needs significant repairs or a tenant stops paying? What governs the distribution of proceeds at sale? These questions are not optional to ask, and in informal arrangements they often go unanswered until something goes wrong. That contractual ambiguity, unclear terms and undefined rights between parties, is itself a concern from a Shariah perspective. Islam places significant emphasis on clarity in financial agreements.

If you are considering this route, the asset should be purchased without any debt, the ownership shares and income distribution method should be documented clearly and the exit terms should be agreed before capital is committed.

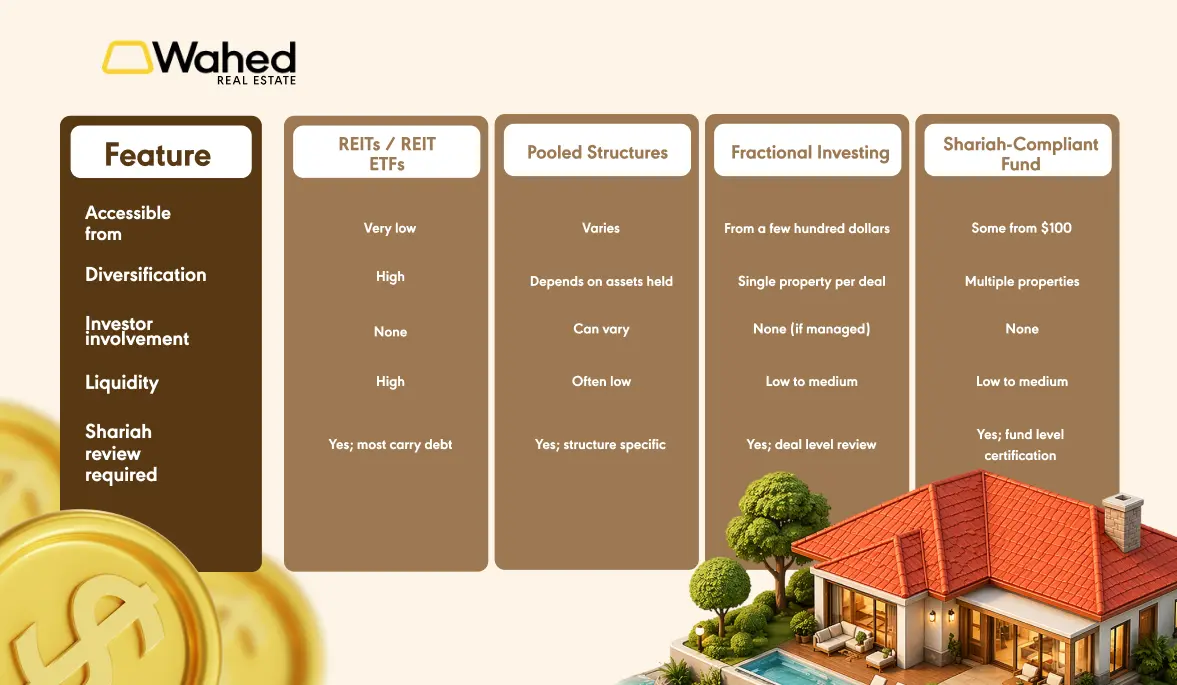

Option 2: REITs and REIT ETFs

A Real Estate Investment Trust is a company that owns income producing properties. Buying shares in a REIT means buying a stake in that company, similar to buying stock in any publicly traded business. By law, REITs must distribute at least 90%2 of their taxable net income to shareholders each year. That legal requirement is what makes them attractive as income investments.

Because REIT shares trade on public exchanges, you can buy in through a standard brokerage account with a small initial outlay. Most publicly traded REITs are priced under $1003 per share, meaning $5,000 gives you meaningful exposure across multiple positions. REIT ETFs bundle exposure to multiple REITs into a single fund, spreading the risk across a larger number of underlying assets.

What to check for Shariah compliance: For Muslim investors, the conversation around REITs tends to focus on one issue: debt. Most conventional REITs carry debt at the portfolio level, which is how they finance property acquisitions. That leverage is baked into the structure and for many scholars, it is enough to make conventional REITs impermissible regardless of what properties they hold.

There are Shariah screened REIT products in the market that attempt to address this. These typically follow AAOIFI standards , which allow for a debt level of up to around 30%4 of a company's market value as one of the criteria for permissibility. The opinions of scholars vary on whether this threshold is sufficient and the debate is a live one in Islamic finance circles. Some consider screened products acceptable with purification of impermissible income. Others maintain that any interest based debt in the structure is a concern that screening ratios do not fully resolve. Where you land on that depends on the scholarly opinion you follow.

What this means practically: if you are looking at a REIT or REIT ETF, the conventional universe is largely set aside. For screened options, the questions to ask are who provided the Shariah certification, what methodology they used, and whether any purification is required on distributions. The label alone is not enough. Independent scholarly certification and a clear compliance framework matter more than what a product calls itself.

Option 3: Fractional Real Estate Investing

Fractional investing lets you own a proportional share of a specific property. Your ownership stake earns a share of the rental income that property generates and a proportional share of any appreciation when it is sold.

Because you are buying a fraction rather than the whole, the capital required is far lower than direct ownership. Some platforms allow investors to participate in individual property deals from as little as $500. With $5,000, you could spread across multiple properties rather than concentrating everything in one.

Wahed offers individual property deals starting from $500, which means $5,000 could give you exposure to up to ten separate properties. Each property goes through an internal investment, compliance and Shariah review process. Properties and tenants are managed professionally, so there are no operational responsibilities for the investor.

Liquidity depends on the platform. Some offer a secondary market where you can list your stake for other investors to buy, though activity on these markets varies and a quick exit is not guaranteed. Others have more structured redemption windows with defined timelines. Either way, fractional real estate is not designed for capital you may need to access at short notice, and the terms differ enough between platforms that it is worth checking before you invest rather than after.

What to watch for Shariah compliance: Fractional real estate is permissible when properties are acquired without any debt, income comes from permitted tenant activity and independent Shariah oversight covers the deal structure.

In the U.S., most fractional platforms hold each property inside its own LLC, with investors receiving membership interests that represent a proportional ownership stake in the underlying asset. When the LLC owns the property with no financing, this maps closely onto Shirkat al-Milk, the Islamic concept of co-ownership where multiple parties hold rights over a shared asset. Scholars generally consider this a good foundation. The concern arises when the LLC carries a mortgage or any debt. At that point, investors' returns are partly generated from a leveraged structure rather than asset ownership, which raises the core Shariah concern.

Option 4: Shariah-Compliant Real Estate Funds

A real estate fund pools investor capital across a portfolio of properties and manages those assets end-to-end through a professional team. Rather than selecting individual deals, investors participate in a broader structure that holds multiple properties.

The main difference from fractional investing is diversification. A single vacancy or an unexpected maintenance issue at one property has a limited effect on an investor’s overall return when it sits alongside many other assets. A fund also removes the need for investors to review individual deals, track assets separately, or make decisions about when to sell.

The Wahed Real Estate Fund is accessible from $100. The fund acquires a portfolio of single-family residential homes across the U.S. entirely with cash, with no debt at any level of the structure. The fund is independently certified by the Shariyah Review Bureau, with ongoing oversight, not just a one-time sign-off.

What to watch for Shariah compliance: The Shariah questions for any real estate fund follow the same logic as other structures, just applied at the fund level rather than the deal level. Does the fund permit leverage? What does the investment mandate allow? Is income derived entirely from permissible sources? Who certifies compliance? These are the questions to ask before investing in any fund that claims Shariah compliance.

Comparing the Four Options

Final Thoughts

$5,000 is a real starting point for halal real estate investing. A house is not on the table at this level. Exposure to income-generating property, through structures built to avoid what Islamic finance prohibits, is.

The four options here carry different trade offs. REITs are accessible and liquid, but most carry debt and need careful screening. Pooled structures vary widely in their legal clarity and governance. Fractional investing offers transparency at the individual asset level, at a lower entry point than direct ownership. A properly structured fund with independent certification provides diversification and professional management without requiring the investor to track deals or make operational decisions.

Across all four, the same three questions apply: is there debt in the structure, who provides independent Shariah oversight, and where does the income come from. Those questions matter more than the minimum investment figure.

Sources:

1 Data provided by the U.S. Census Bureau and the U.S. Department of Housing and Urban Development, accessed via FRED®.

2 Cohen & Co, accessed March 2026.

3 The Motley Fool, “How to Invest in Real Estate Investment Trusts (REITs) in 2026”, accessed May 2026.

4 AAOIFI Shariah Standards, accessed May 2026.

Disclosure

This article is for educational and informational purposes only. It does not constitute financial, investment,legal, or religious advice. Wahed Financial, LLC ("Wahed"), as a manager of Wahed Real Estate Fund I LLC; Wahed Real Estate Series I, LLC (the “Wahed Issuer”), operates the wahed.com/real-estate website (the "Site") and is not a broker-dealer or investment advisor. All securities related activity is conducted through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC, located at 525 Green Place, Woodmere, NY 11598.

This investment is speculative, illiquid and involves substantial risk, including the possible loss of your entire investment. Securities are offered through Dalmore Group LLC, Member FINRA/SIPC. Wahed and Dalmore are not affiliates. Investors will be clients of Wahed. An offering statement has been filed with the SEC. SEC qualification does not imply approval or endorsement of the offering’s merits. Please review the full offering circular for complete terms and risks.

Investors are purchasing shares of a Fund and not the underlying asset(s) of the Fund. There is no assurance any Fund will achieve its objectives, is not listed on an exchange and may not be suitable for all investors. Distributions are subject to and are not guaranteed.