.jpeg)

Key Takeaways:

Real estate has always been one of the most trusted ways to build long-term wealth. For Muslim investors, the appeal is easy to see. It is a physical asset you can understand. But the question is never just whether to invest in real estate. It is how to do it in a way that is Shariah compliant.

The U.S. real estate market is worth roughly $3.5 trillion¹ but it is built on interest-based debt. Between conventional mortgages and complex financial products, many common paths are off limits for those looking for halal returns.

The good news is that the landscape has changed. More halal real estate investment options exist in the U.S. today than ever before.You can now find options that fit your budget while sticking to Shariah principles.

This guide walks through the main real estate investing options in the U.S. and explains the Shariah details you need to know.

What Makes a Real Estate Investment Halal?

Before looking at specific options, we have to look at what makes an investment Shariah-compliant. It is about more than just avoiding interest. The 7 key pillars to consider are:

- Real asset ownership: Investments must be connected to a tangible, physical property, not to financial instruments detached from any real asset.

- Rental income as the source of return: Earning rent from tenants who use a property for lawful purposes is one of the clearest forms of halal income. It is a genuine exchange of value.

- No riba: Riba means interest. Any structure relying on interest-bearing debt, at the property level, the fund level, or in how returns are generated, raises serious Shariah concerns.

- No prohibited leverage: Using interest-bearing loans to boost returns is not allowed under Shariah. A more permissible option uses asset-backed structures instead.

- Tenant activity screening: Income from tenants in prohibited businesses, such as liquor stores or gambling, is not halal even if the property was purchased cleanly.

- Independent Shariah oversight: A self-declared halal label is not the same as independent certification by qualified scholars. Look for investments that are reviewed and certified by qualified Shariah scholars.

- Purification: In complex structures where a small portion of income may be borderline. In these cases, scholars advise donating that proportion to charity rather than consuming it.

Why Many Muslim Investors Choose to invest in Real Estate

For many in our community, real estate is a natural way to grow wealth. It offers a combination of tangible assets, passive rental income and long-term appreciation that aligns with Islamic values.

In Islamic tradition, property and fixed assets are seen as productive forms of wealth because they are tied to real economic activity. That makes real estate one of the more natural fits for Muslims who want to invest in real estate, Islamically, without compromising on their values. According to recent data by FRED², national home prices have reached $403,200 as of May 2026. Since 1995, residential property values have grown by 309%³, proving its resilience over several decades.

Even through various market shifts, residential real estate has maintained an average annual growth rate of 6.2%⁴ over the last 25 years.

Historically, accessing that growth in a shariah compliant way meant either buying property outright in cash or sitting on the sidelines. Fortunately, the landscape is changing. A new range of halal real estate alternatives are now available in the market. Below, we discuss these options in detail to help you understand how they work.

Your Guide to Halal Real Estate Investment Options in the U.S. for 2026

1. Direct Property Ownership

Buying a property outright with cash and earning rental income from tenants is the most straightforward form of halal real estate investing. This approach involves no debt, no interest and no structural complexity. You own the asset, you collect the rent, and over time you benefit from property value appreciation.

The main challenge is access. With the median U.S. home now above $403,000², buying outright in cash requires substantial capital that most investors do not have. Add the operational burden of being a landlord, maintenance, vacancies, tenant disputes, and the time commitment becomes significant. Direct ownership rewards those with capital, experience and patience. For most people starting out, it is often an aspirational goal rather than a first step.

From a Shariah perspective, a cash-purchase for direct ownership is one of the cleanest structures available because the concern of riba is removed at the source. However, ongoing compliance still requires attention. You must ensure proper tenant screening to confirm the property is being used for a lawful purpose.

2. REITs and REIT ETFs

Real Estate Investment Trusts (REITs) are companies that own and operate income-producing properties. They allow you to buy shares in the real estate market just like you would buy stocks in any other company. REITs are popular because they are required by law to distribute at least 90% of their taxable income to shareholders, usually in the form of dividends. You can buy them through a standard brokerage account, and because they trade on public exchanges, you can sell your shares whenever the market is open.

While REITs are easy to access, they are often complicated for Muslim investors. Most conventional REITs use a high amount of interest-bearing debt to buy and manage their properties. They may also lease space to tenants in prohibited industries like gambling or alcohol.

There are options in the market labeled as Shariah-compliant, but it is important to understand how they work. Most of these products are not completely debt-free. Instead, they use specific screening methodologies, such as those set by AAOIFI (Accounting and Auditing Organization for Islamic Financial Institutions), which allow for limited amounts of interest-based debt - typically capped at 30%⁵ of the company's market capitalization. These thresholds vary by Shariah screening methodology. Additionally, any small incidental income from non-permissible sources must be monitored and requires "purification," which means donating that portion of your earnings to charity.

Because structures vary, you should always check for independent Shariah certification before investing.

3. Islamic Home Financing Products

Some home-financing products are often marketed as Shariah-compliant alternatives to conventional mortgages. Structures can vary widely and may involve co-ownership arrangements, lease structures or installment purchase agreements rather than traditional interest-based lending. The most commonly cited examples in the U.S. market are Murabahah, Ijarah and Diminishing Musharakah.

Scholarly acceptance of these structures varies considerably. Even when a product attempts to avoid explicit interest, the economic outcomes and pricing often closely resemble conventional debt. Because the risk and cash flow profiles can mirror a standard mortgage, these products are generally less ideal for those seeking a pure investment.

Most importantly, these products are designed for purchasing a home to live in, not for building a diversified portfolio. They should be viewed as a financing solution rather than a real estate investment strategy. If you do consider this path, a careful review of the contracts and the quality of Shariah oversight is essential.

4. Fractional Real Estate Investing

Fractional investing allows a group of investors to pool their resources to collectively own shares in a property. This lowers the barrier to entry significantly. It gives you real exposure to specific real estate assets without needing the massive capital that direct ownership demands. It is an ideal entry point for those who want to understand exactly which assets they are participating in and build their portfolio deal by deal.

In practice, platforms like Wahed allow you to access individual property deals starting from $500. You buy a fractional share in a specific property, earn potential rental income proportional to your ownership stake and benefit from any appreciation when the property is eventually sold. There is no operational burden for the investor as the properties and tenants are managed professionally.

How easily you can exit your investment depends on the specific platform’s secondary market and demand. As with most real estate, liquidity is generally limited, so you should plan for a medium-term investment horizon rather than treating this as liquid cash. From a Shariah perspective, fractional real estate is halal when properties are purchased without debt and each deal undergoes strict review, as is the case with Wahed's internal compliance and Shariah oversight.

5. Shariah-Compliant Real Estate Funds

A Shariah-compliant real estate fund pools investor capital and deploys it across a portfolio of properties managed by a professional investment team. Instead of owning one house, you gain proportional exposure to an entire diversified portfolio. This structure is designed to remove the biggest barriers many face: high capital requirements, complex management and unclear Shariah governance.

Wahed Real Estate is a practical example of this approach. Starting from $100, making it one of the most accessible real estate investment structures available. Every property is purchased with 100% cash. No mortgages, no debt. Income comes entirely from residential tenant rents, potentially distributed to investors quarterly.

While real estate is generally a long-term asset, it offers specific exit windows. After an initial six-month holding period, investors can request withdrawals during semi-annual windows. From a Shariah perspective, the 100% equity structure eliminates riba at the source. It is also reviewed and certified by the Shariyah Review Bureau (SRB), providing independent oversight throughout the life of the investment.

This option suits investors who want professional management, diversification and passive halal rental income without the operational responsibilities of direct or fractional property management.

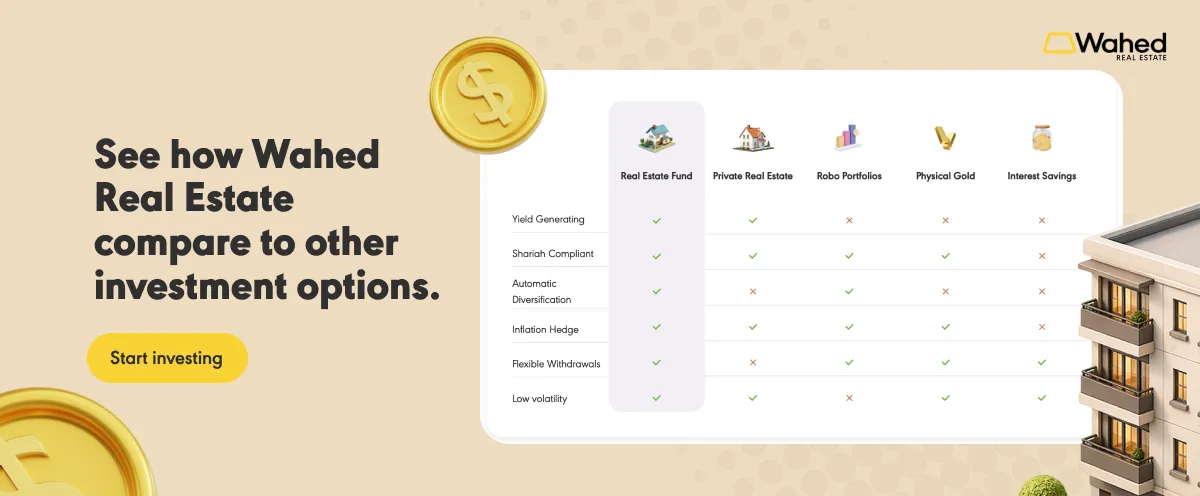

Comparing Your Options

What to Look for in a Halal Real Estate Investment

Before committing to any real estate product, use this checklist to guide your review:

- Is the structure equity-based or debt-based? The most important question. No interest at any level of the structure is the gold standard.

- Who provides Shariah oversight? Independent certification by recognized scholars carries more weight than an internal stamp of approval.

- Where does the income come from? Ensure returns are derived from rent paid by real tenants rather than interest or opaque financial instruments.

- What is the minimum investment? Check if the product is accessible to retail investors or restricted to accredited, high-net-worth individuals.

- What are the liquidity terms? Always understand redemption windows, lock-up periods, and exit fees before you invest.

- Who manages the portfolio? Look for professional management teams with a demonstrable track record in real estate.

How Wahed Approaches Halal Real Estate Investing

Wahed offers two routes into halal real estate investing for U.S. investors, and they are designed to complement each other depending on where you are in your investing journey.

The first is individual property deals through fractional investing, starting from $500. This suits investors who want to choose specific assets, understand exactly what they own, and build their portfolio deal by deal.

The second is through Wahed Real Estate, starting from $100. This is for investors who want a simpler, more hands-off approach. Rather than picking individual deals, you get exposure to a professionally managed, diversified portfolio. It handles acquisitions, property management, tenant relations and distributions.

Final Thoughts

For Muslim investors in the U.S., the options for halal real estate investing have improved. Direct ownership remains the cleanest structure for those with the capital. REITs offer accessibility and liquidity, but require careful Shariah awareness. Home financing products serve home buyers, not investors. Fractional investing opens up specific deals at a lower entry point. And a properly structured Shariah-compliant real estate fund brings professional management, diversification and passive income together in one place.

What separates a sound halal investment from a poorly structured one is not always obvious. It comes down to what the structure is built on, who provides the oversight and whether income is derived from permissible sources. Those questions are worth asking carefully before committing any capital.

Sources:

¹ Expert Market Research (2026), “United States Real Estate Market Size, Share, Growth,” https://www.expertmarketresearch.com/reports/united-states-real-estate-market

² Federal Reserve Bank of St. Louis (2026), “Median Sales Price of Houses Sold for the United States,” https://fred.stlouisfed.org/series/MSPUS

³ iPropertyManagement (2025), “Average ROI of Real Estate,” https://ipropertymanagement.com/research/real-estate-roi

⁴ Board of Governors of the Federal Reserve System (2025), “Financial Stability Report,” https://www.federalreserve.gov/publications/April-2025-financial-stability-report-Asset-Valuations.htm

⁵ Halal Ninja (2020), “The AAOIFI Standard For Halal Investing,” https://halal.ninja/what-is-aaoifi

Disclaimer:

Risk Disclosure: Wahed Financial, LLC ("Wahed"), as a manager of Wahed Real Estate Series I, LLC (the “Wahed Issuer”), operates the wahed.com/real-estate website (the "Site") and is not a broker-dealer or investment advisor. All securities related activity is conducted through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC, located at 525 Green Place, Woodmere, NY 11598. You can review the brokercheck for Dalmore. An up-to-date Dalmore Form CRS is available. You should speak with your financial advisor, accountant and/or attorney when evaluating any offering. Neither Wahed, the Wahed Issuer, nor Dalmore makes any recommendations or provides advice about investments, and no communication, through this website or in any other medium, should be construed as a recommendation for any security offered on or off this investment platform.

This Site may contain forward-looking statements and information relating to, among other things, Wahed, the Wahed Issuer, their respective business plans and strategies, and their industry. These forward-looking statements are based on the beliefs of, assumptions made by, and information currently available to Wahed and its management. When used in the Site, the words “estimate,” “project,” “believe,” “anticipate,” “intend,” “expect” and similar expressions are intended to identify forward-looking statements, which constitute forward-looking statements. These statements reflect Wahed management’s current views with respect to future events and are subject to risks and uncertainties that could cause the Wahed Issuer’s actual results to differ materially from those contained in the forward-looking statements. You should not rely on these statements but should carefully evaluate the offering materials in assessing any investment opportunity, including the complete set of risk factors that are provided as part of the offering circular for your consideration. Investors are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. Wahed and the Wahed Issuer do not undertake any obligation to revise or update these forward-looking statements to reflect events or circumstances after such date or to reflect the occurrence of unanticipated events.

The Wahed Issuer is conducting one or more offerings, pursuant to Regulation A of the Securities Act of 1933, as amended (“Regulation A”), of interests in separate series established to hold residential properties to be acquired by such series. The offering circular and periodic reports for the Wahed Issuer are available on our Filings Page (https://www.sec.gov/Archives/edgar/data/2092195/000121390025100303/ea0258093-1a_wahed1.htm). An investment in a series constitutes only an investment in that particular series and not in the Wahed Issuer or the underlying asset(s) of that or any other series. From time to time, the Wahed Issuer may seek to qualify additional series offerings under Regulation A. For offerings that have not yet been qualified, no money or other consideration is being solicited and, if sent in response, will not be accepted. No offer to buy securities of a particular offering can be accepted, and no part of the purchase price can be received, until an offering statement filed with the Securities and Exchange Commission (the "SEC") relating to that series has been qualified by the SEC. Any such offer may be withdrawn or revoked, without obligation or commitment of any kind, at any time before notice of acceptance given after the date of qualification by the SEC. An indication of interest involves no obligation or commitment of any kind. You may obtain a copy of the Wahed Issuer’s offering circular at [https://www.sec.gov/Archives/edgar/data/2092195/000121390025100303/ea0258093-1a_wahed1.htm].

Please review the offering circular and the documents included as exhibits to the related offering statement before making any investment decision.

Investment overviews contained herein contain summaries of the purpose and the principal business terms of the investment opportunities. Such summaries are intended for informational purposes only and do not purport to be complete, and each is qualified in its entirety by reference to the more-detailed discussions contained in the offering circular filed with the SEC. The Wahed Issuer does not offer refunds after an investment has been made. Please review the offering circular and other offering materials for more information.

An investment in any series is illiquid and speculative. The Wahed Issuer does not have a redemption provision and, as a result, if a series does not successfully dispose of its real estate, you may have to hold your investment in that series for an indefinite period. An active trading market for series interests of any series may not develop or be sustained. If an active public trading market for such series interests does not develop or is not sustained, it may be difficult or impossible for you to resell your series interests at any price. Even if an active market does develop, the market price could decline below the amount you paid for your series interests.