Key Takeaways:

For Muslim professionals in the U.S. building retirement wealth, zakat on investment accounts is one of the most practically important - and most commonly misunderstood - questions in Islamic personal finance.

You know Zakat applies to cash savings, gold, and business assets. But what about your IRA? Your 401(k)? Funds you legally own but can't touch for decades without penalty? Do they count as zakatable wealth?

The honest answer is that scholarly opinions differ - and understanding both positions will help you make an informed decision aligned with your values and your financial reality.

What Is Zakat and Why It Matters in Wealth Management

Zakat is one of the five pillars of Islam - an annual obligatory contribution on qualifying wealth, distributed to those in need. It is not optional sadaqa (voluntary charity); it is a religious duty for every Muslim whose wealth exceeds the nisab threshold and has been held for one full lunar year (hawl).

The rate is fixed: 2.5% of all zakatable net assets after deducting zakatable liabilities.

The nisab is the minimum threshold of wealth that triggers the zakat obligation. It is calculated based on either the current value of 87.48 grams of gold or 612.36 grams of silver - whichever methodology your scholar advises. Because precious metal prices fluctuate, the nisab threshold changes annually. Many Islamic finance organisations publish updated nisab values at the start of each Ramadan.

For most Muslim professionals in the $80K-$250K income range who hold retirement accounts, the nisab question is rarely the issue - the accounts almost certainly exceed the threshold. The real question is: which retirement assets count, and how are they calculated?

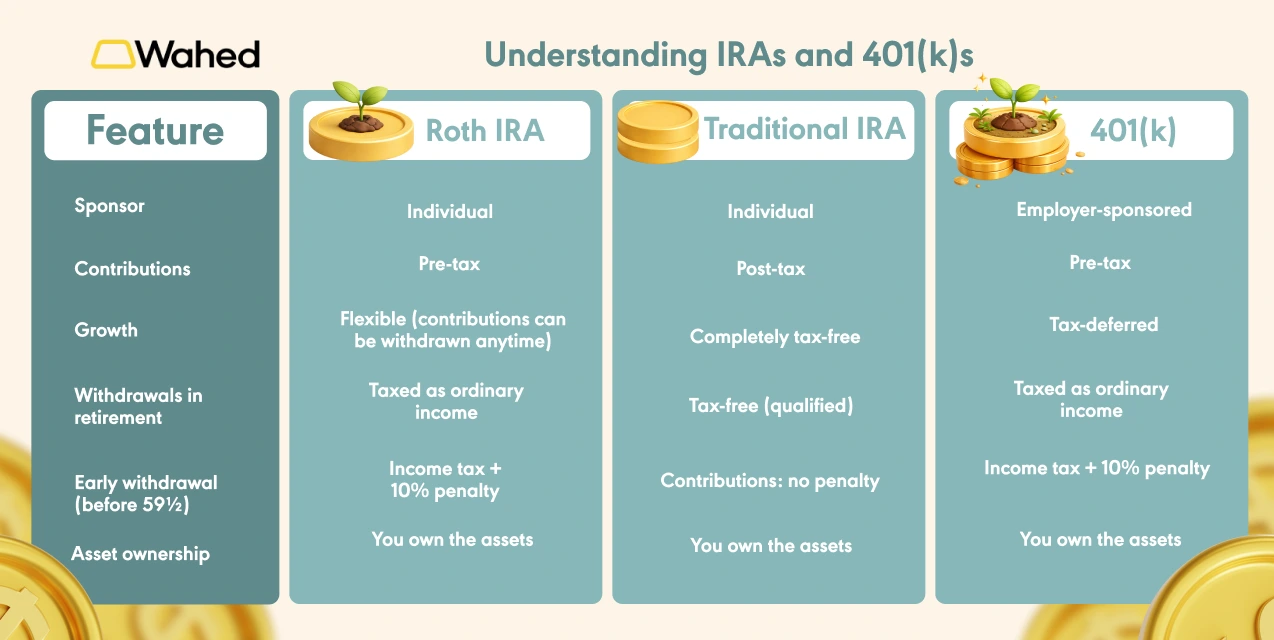

Understanding IRAs and 401(k)s

Before addressing the zakat question directly, it helps to be clear on what these accounts actually are.

A Traditional IRA allows pre-tax contributions that grow tax-deferred. Withdrawals in retirement are taxed as ordinary income. Early withdrawals (before age 59½) incur both income tax and a 10% penalty¹.

A Roth IRA accepts post-tax contributions and grows completely tax-free. Qualified withdrawals in retirement are tax-free. Contributions (not earnings) can be withdrawn at any time without penalty², but earnings face restrictions before 59½.

A 401(k) is employer-sponsored and operates similarly to a Traditional IRA in terms of zakat treatment - pre-tax contributions, tax-deferred growth, taxable withdrawals, and early withdrawal penalties before 59½³.

All three are investment accounts: you own the assets inside them. The U.S. government imposes tax rules and withdrawal restrictions, but the wealth legally belongs to you. That ownership question is central to the scholarly debate.

Do Muslims Have to Pay Zakat on Retirement Accounts?

This is where contemporary Islamic scholarship acknowledges genuine complexity. Unlike cash in a bank account - freely accessible at any time - retirement accounts carry restrictions that affect the classical concept of tamam al-milk, or complete ownership.

Two main scholarly positions have emerged, and both have credible support. Rather than asserting one as definitively correct, understanding each allows you to consult your own scholar and make an informed decision.

View 1: Zakat Is Due Only When Funds Are Accessible

A significant number of contemporary scholars hold that zakat on retirement accounts is only obligatory at the point of withdrawal - not annually while the funds remain locked.

The reasoning: Classical zakat jurisprudence requires that wealth be fully owned and accessible. Retirement accounts before the withdrawal age carry meaningful restrictions: early withdrawal triggers a 10% federal penalty on top of ordinary income tax, creating a substantial barrier that did not exist in classical conceptions of owned wealth. Some scholars argue that restricted assets - those you cannot freely use without financial consequence - do not meet the threshold for full zakatable ownership.

The practical implication: Under this view, you would calculate and pay zakat on retirement funds in the year you actually withdraw them - on the net amount received after taxes and penalties. No annual zakat payment would be due on locked IRA or 401(k) balances while they remain in the account.

This position is favoured by scholars who apply classical fiqh principles conservatively to modern financial instruments.

View 2: Zakat Is Due Annually on Retirement Savings

An equally prominent scholarly position holds that zakat is due each year on retirement account balances, because the fundamental criteria for zakatable wealth - ownership and growth - are both clearly present.

The reasoning: You are the legal and beneficial owner of your IRA or 401(k). The account value grows for your direct benefit. Withdrawal restrictions are a legal administrative feature, not a negation of ownership - just as other liquid assets you choose not to sell still attract zakat. Furthermore, if you did choose to withdraw the funds (with penalty), you could. The choice exists, even if it is financially unfavourable.

The practical method: Calculate zakat annually on the current market value of your retirement account - either on the full balance, or on the net value after estimated taxes (discussed below in the calculation section).

This view is adopted by several Islamic finance organisations and zakat houses in the U.S., particularly for accounts where early withdrawal is technically possible even if penalised.

How to Calculate Zakat on an IRA

If you follow View 2 and calculate zakat annually, there are two accepted methods for determining the zakatable base.

Method 1: Calculate Zakat on the Full Portfolio Value

This is the simpler approach. You take the current market value of your IRA or 401(k) and apply the standard 2.5% zakat rate.

This method is more conservative - it errs on the side of generosity and avoids the complexity of estimating future tax liabilities. Some scholars prefer it precisely for that reason.

Method 2: Calculate Zakat on the Net Withdrawable Value After Taxes

This approach accounts for the fact that a portion of your IRA balance will never be yours in practice - it belongs to the government in the form of deferred income tax. Calculating zakat on the gross balance, some argue, means paying zakat on wealth you don't actually own.

Under this method, you deduct your estimated tax liability (and any applicable penalty if you're under 59½) from the gross account value, then apply the 2.5% zakat rate to the net accessible amount.

For a Roth IRA, since qualified withdrawals are tax-free, the full balance is typically used as the zakatable base under both methods.

Example: Zakat Calculation on a Retirement Account

Consider a Muslim professional with a Traditional IRA valued at $100,000 and an estimated effective tax rate of 25% at retirement.

Method 1 - Full portfolio value:

Method 2 - Net withdrawable value (at retirement age, no penalty):

If under age 59½ (early withdrawal scenario)

The difference between methods is meaningful - ranging from $1,625 to $2,500 on a $100,000 account. Over a $300,000-$500,000 retirement portfolio, which is not uncommon for the ICP of this article, the divergence becomes significant: roughly $5,000-$12,500 in annual zakat depending on method and account size.

Neither method is definitively "correct" - both have scholarly support. What matters is that you are consistent year to year and that your approach is grounded in a clear scholarly opinion, ideally one you have specifically discussed with a knowledgeable Islamic finance scholar.

Managing Wealth the Halal Way

Zakat is not just a financial obligation - it is an act of worship and one of the most visible expressions of the Islamic relationship between wealth and responsibility. For Muslim professionals building retirement savings in the U.S., ensuring that zakat is calculated thoughtfully and paid on time is as much a part of responsible wealth management as choosing the right investments.

The two dimensions go together.

Sources:

¹ GE Credit Union (2022), “Your Guide to Traditional IRA Withdrawal Rules,” https://www.gecreditunion.org/learn/education/resources/money-minutes/march-2022/your-guide-to-traditional-ira-withdrawal-rules

² BlackRock (2025), “Withdrawal Rules and Strategies,” https://www.blackrock.com/us/individual/education/retirement/withdrawal-rules-and-strategies

³ Investopedia (2024), “How 401(k) Withdrawals Work When You're Unemployed,” https://www.investopedia.com/articles/insights/073116/how-401k-withdrawals-work-when-youre-unemployed.asp

Disclaimer:

* For illustrative purposes only and is not intended to represent results of a real investment. 7% hypothetical return shown is based on historical averages. Rates of return vary of time.

This article is for educational purposes only and does not constitute religious, financial, tax or legal advice. Scholarly opinions on zakat and retirement accounts vary. We recommend consulting a qualified Islamic scholar or mufti for guidance on your specific situation. Investment involves risk, including loss of principal. Past performance is not indicative of future results. Wahed Invest LLC is a registered investment adviser with the SEC. The term halal denotes that permissibility in accordance with Islamic law. Wahed Invest does not provide tax advice.

Wahed Invest does not provide tax advice and this should not be considered tax advice. Tax laws and regulations are subject to change. When taking withdrawals from an IRA before age 59½, you may have to pay ordinary income tax plus a 10% federal penalty tax. Withdrawals from a Roth IRA are tax-free if you are over age 59½ and have held the account for at least five years; withdrawals taken prior to age 59½ or five years may be subject to ordinary income tax or a 10% federal penalty tax, or both. Consult a tax professional regarding your specific situation.