Key Takeaways:

Real estate sits at the top of the wealth-building list for many Muslim professionals in the U.S. - and for good reason. Property offers passive income, inflation protection, and a tangible asset that doesn't fluctuate with daily market sentiment the way stocks do. But the question of whether it's Shariah-compliant is more nuanced than a simple yes or no.

The short answer: Real estate investing is generally halal in principle. Owning property, earning rental income, and building wealth through real assets is entirely consistent with Islamic finance. The question of compliance comes down to structure - specifically, how the property is financed and how income is generated from it.

Why Many Muslims Consider Investing in Real Estate

Property has long been considered one of the most reliable wealth-building vehicles available to individuals. For Muslim professionals earning $80K-$300K with growing net worth and a desire to diversify beyond equities, real estate can offer several distinct advantages.

Passive income potential. A rental property can generate monthly cash flow from tenants - income that requires no active daily effort once the property is acquired and managed. For professionals with high earning potential but limited time, this passive income structure is attractive.

Diversification beyond stocks. Real estate has a low correlation with equity markets - property values and rental income don't necessarily move in step with S&P 500 fluctuations. For Muslim investors already holding halal equity portfolios, real estate adds a different return profile and a hedge against stock market volatility.

Tangible asset ownership. Unlike a share in a company, real estate is a physical asset with intrinsic utility. Land and buildings have been typically recognised as legitimate wealth under Islamic jurisprudence for centuries. In general, there is nothing speculative about owning a property that houses families, businesses, or communities.

Long-term appreciation. U.S. real estate has historically appreciated over long time horizons, particularly in urban and suburban markets with strong employment bases. Combined with potential rental income, the total return profile makes property a meaningful component of a long-term halal wealth strategy.

Islamic Principles That Apply to Real Estate Investing

The same Islamic finance framework that governs equity investing applies to real estate - with specific implications for how property is acquired and how income is structured.

Prohibition of riba (interest). The most consequential principle for real estate in the U.S. Conventional property financing relies entirely on interest-bearing mortgages - a fixed or variable interest rate applied to a loan balance over 15-30 years. This is riba, and it is the primary compliance issue for Muslim real estate investors. The property itself is not the problem; the conventional financing mechanism is.

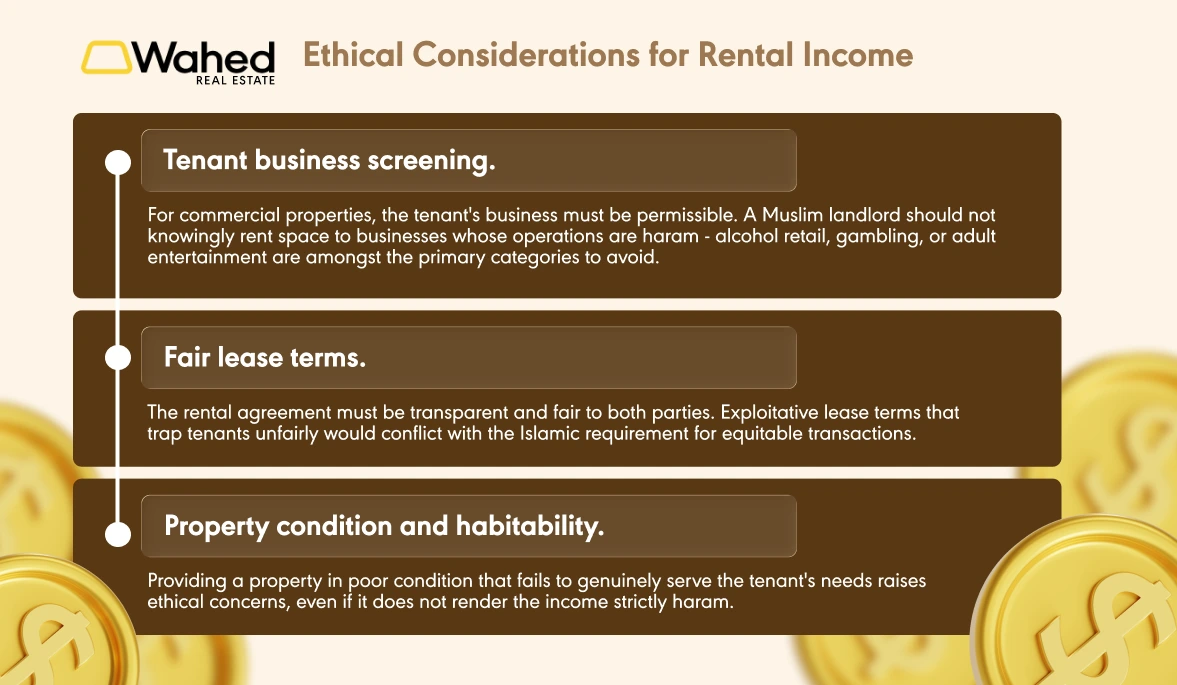

Avoidance of haram business activities. A property you own must not generate income from tenants whose business is impermissible under Shariah. Renting a commercial unit to a liquor store, casino, or adult entertainment venue is not permissible, even if the property itself is legitimate. The rental income would be contaminated by the haram source.

Fair and ethical transactions. Islamic finance requires transparency, mutual consent, and the absence of gharar (excessive uncertainty or deception) in contracts. This applies to lease terms, tenant agreements, and any investment partnership structures.

Is Rental Income Halal?

Yes, rental income is generally permissible under Islamic finance, and it is one of the cleanest income structures available to Muslim investors.

The reason is straightforward: rental income is asset-based. You own a property, you provide shelter or commercial space of genuine utility, and tenants pay for that use. The income derives from the productive use of a real asset, not from lending money at interest. This asset-based income structure - where wealth is generated through real economic activity - is precisely what Islamic finance encourages.

The ethical considerations are relatively narrow:

For residential rental properties let to Muslim or non-Muslim tenants for ordinary living purposes, the income is straightforwardly halal.

Are REITs Halal?

Real Estate Investment Trusts (REITs) are publicly traded companies that own and operate income-generating real estate - office buildings, residential complexes, shopping centres, warehouses, data centres, and more. They are required by U.S. law to distribute at least 90% of taxable income to shareholders¹, making them popular income vehicles.

The halal status of REITs is not straightforward, and it requires the same Shariah screening applied to stocks and ETFs.

Why conventional REITs are often not halal:

Most conventional REITs carry significant interest-bearing debt - leverage ratios of 40–60% of property value are common². Under standard Shariah financial ratio screens, interest-bearing debt around 33% of total assets or market capitalization renders a company non-compliant. Many REITs fail this test. Thresholds may vary depending on different Shariah screening methodologies and interpretations across scholars and screening providers.

Additionally, some REITs own properties whose tenants operate haram businesses - hotels with bars and casinos, entertainment venues, and so on. The REIT's income would be partially derived from those tenants.

Conditions under which REITs may be permissible:

A REIT can pass Shariah screening if it meets the same criteria as any other equity investment: low debt ratios, predominantly halal tenant mix, and limited non-compliant revenue. Some industrial and logistics REITs - warehouses, data centres, logistics hubs - have lower leverage and less exposure to haram tenants, making them more likely to pass screening.

Shariah-compliant REIT structures also exist, where the fund is specifically designed around Islamic finance principles from the outset - no interest-based financing, no haram tenant categories, and Shariah board oversight.

For Muslim investors interested in real estate investment trusts, the key is not to assume any REIT is halal by default - it requires the same sector and financial ratio analysis applied to individual stocks in addition to the continued monitoring for Shariah-compliance.

Halal Ways to Invest in Real Estate

For Muslim professionals in the U.S., three practical structures provide genuine, Shariah-compliant real estate exposure.

Direct Property Ownership

Purchasing a rental property outright is the most direct halal real estate investment. You own the asset, collect rental income, and benefit from long-term appreciation. The compliance requirements are: Shariah-compliant ownership (not a conventional mortgage), halal tenants, and fair lease terms.

For investors with sufficient capital, direct ownership is the cleanest structure available.

Real Estate Partnerships and Syndications

Real estate syndications pool capital from multiple investors to acquire larger properties - apartment blocks, commercial buildings, industrial facilities - that individual investors could not purchase alone. Structured as musharakah (equity partnership), where investors share ownership, risk, and profit proportionally, syndications can be fully Shariah-compliant.

The key due diligence questions: Is the acquisition financed through interest or debt bearing structures? What is the property used for? How is income distributed - as profit-sharing or through instruments that resemble interest?

Joint investment partnerships structured around genuine co-ownership and profit-sharing - rather than fixed interest-like returns - are consistent with Islamic finance.

Shariah-Compliant Real Estate Funds

Managed real estate funds built on Islamic finance principles offer diversified property exposure without the concentration risk of owning a single property. These funds invest across multiple properties and geographies, providing the diversification benefits of REITs with the compliance assurance of Shariah oversight.

For investors who want real estate exposure in their portfolio without the operational responsibility of direct property management, Shariah-compliant real estate funds are the most accessible entry point.

Building Wealth the Halal Way

Real estate is one of the most powerful long-term wealth-building tools available - and it is fully accessible to Muslim investors in the U.S. who understand the structures that make it compliant.

The question is not whether property investing fits within an Islamic finance framework. It does. The question is choosing structures that reflect your values: asset-based income over interest income, genuine ownership over debt, fair transactions over exploitation.

Sources:

¹ Intuit TurboTax (2025), Tax Tips for Real Estate Investment Trusts. https://turbotax.intuit.com/tax-tips/investments-and-taxes/tax-tips-for-real-estate-investment-trusts/L0tW3ad6C

² DoorLoop (2026), REITs Statistics: Key Trends In 2026. https://www.doorloop.com/blog/reits-statistics

Disclosure:

Risk Disclosure: For U.S. audience. This article is for educational purposes only and does not constitute financial, legal, or religious advice. Islamic finance rulings on specific structures may vary by scholarly opinion. We recommend consulting a qualified Islamic scholar and financial adviser for guidance on your specific situation.

This investment is speculative, illiquid and involves substantial risk, including the possible loss of your entire investment. Securities are offered through Dalmore Group LLC, Member FINRA/SIPC. Wahed and Dalmore are not affiliates. Investors will be clients of Wahed. An offering statement has been filed with the SEC. SEC qualification does not imply approval or endorsement of the offering’s merits. Please review the full offering circular for complete terms and risks.

Wahed Financial, LLC ("Wahed"), as a manager of Wahed Real Estate Fund I LLC (the “Wahed Issuer”), operates the wahed.com/real-estate website (the "Site") and is not a broker-dealer or investment advisor. All securities related activity is conducted through Dalmore Group LLC, a registered broker-dealer and member of FINRA/SIPC, located at 525 Green Place, Woodmere, NY 11598. You can review the brokercheck for Dalmore. An up-to-date Dalmore Form CRS is available. You should speak with your financial advisor, accountant and/or attorney when evaluating any offering. Neither Wahed, the Wahed Issuer, nor Dalmore makes any recommendations or provides advice about investments, and no communication, through this website or in any other medium, should be construed as a recommendation for any security offered on or off this investment platform. This Site may contain forward-looking statements and information relating to, among other things, Wahed, the Wahed Issuer, their respective business plans and strategies, and their industry. These forward-looking statements are based on the beliefs of, assumptions made by, and information currently available to Wahed and its management. When used in the Site, the words “estimate,” “project,” “believe,” “anticipate,” “intend,” “expect” and similar expressions are intended to identify forward-looking statements, which constitute forward-looking statements. These statements reflect Wahed management’s current views with respect to future events and are subject to risks and uncertainties that could cause the Wahed Issuer’s actual results to differ materially from those contained in the forward-looking statements. You should not rely on these statements but should carefully evaluate the offering materials in assessing any investment opportunity, including the complete set of risk factors that are provided as part of the offering circular for your consideration. Investors are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date on which they are made. Wahed and the Wahed Issuer do not undertake any obligation to revise or update these forward-looking statements to reflect events or circumstances after such date or to reflect the occurrence of unanticipated events.

The Wahed Issuer is conducting one or more offerings, pursuant to Regulation A of the Securities Act of 1933, as amended (“Regulation A”), of interests in separate fund established to hold residential properties to be acquired by such fund. The offering circular and periodic reports for the Wahed Issuer are available on our Filings Page. An investment in a fund constitutes only an investment in that particular fund and not in the Wahed Issuer or the underlying asset(s) of that or any other fund. From time to time, the Wahed Issuer may seek to qualify additional fund offerings under Regulation A. For offerings that have not yet been qualified, no money or other consideration is being solicited and, if sent in response, will not be accepted. No offer to buy securities of a particular offering can be accepted, and no part of the purchase price can be received, until an offering statement filed with the Securities and Exchange Commission (the "SEC") relating to that fund has been qualified by the SEC. Any such offer may be withdrawn or revoked, without obligation or commitment of any kind, at any time before notice of acceptance given after the date of qualification by the SEC. An indication of interest involves no obligation or commitment of any kind. You may obtain a copy of the Wahed Issuer’s offering circular here.

Please review the offering circular and the documents included as exhibits to the related offering statement before making any investment decision. Distributions are subject to change and are not guaranteed.

Investment overviews contained herein contain summaries of the purpose and the principal business terms of the investment opportunities. Such summaries are intended for informational purposes only and do not purport to be complete, and each is qualified in its entirety by reference to the more-detailed discussions contained in the offering circular filed with the SEC. The Wahed Issuer does not offer refunds after an investment has been made. Please review the offering circular and other offering materials for more information.

An investment in any fund is illiquid. The Wahed Issuer does not have a redemption provision and, as a result, if a fund does not successfully dispose of its real estate, you may have to hold your investment in that fund for an indefinite period. An active trading market for fund interests of any fund may not develop or be sustained. If an active public trading market for such fund interests does not develop or is not sustained, it may be difficult or impossible for you to resell your fund interests at any price. Even if an active market does develop, the market price could decline below the amount you paid for your fund interests.