Key Takeaways:

Should Muslim Parents in the U.S. Open a Custodial Investment Account?

One of the most meaningful financial decisions a Muslim parent can make is not about their own retirement or their next property - it's about the head start they give their children. Investing on behalf of a child before they reach adulthood is one of the clearest expressions of the Islamic concept of amanah: responsible stewardship of what you've been given, in service of those who come after you.

In the U.S., the primary legal vehicle for investing on a child's behalf is a custodial investment account — specifically a UGMA or UTMA account. This guide explains how they work, whether they align with Islamic principles, how they compare to education savings plans like 529s, and how Muslim parents can use them to build meaningful wealth for their children starting today.

What Is a Custodial Investment Account?

A custodial investment account is a brokerage account opened by an adult (the custodian - usually a parent or grandparent) on behalf of a minor child (the beneficiary). The custodian manages the account and makes all investment decisions until the child reaches the age of majority - typically 18 or 21 depending on the state.

At that point, the assets transfer irrevocably to the child, who then owns and controls the account outright. This transfer is permanent: once assets are placed in a custodial account, they legally belong to the child and cannot be reclaimed by the parent.

Two federal laws govern these accounts in the U.S.:

UGMA (Uniform Gifts to Minors Act) covers financial assets - stocks, bonds, mutual funds, ETFs, and cash. Available in all 50 states, UGMA accounts are the more widely used structure and the standard choice for parents investing in diversified portfolios.

UTMA (Uniform Transfers to Minors Act) covers a broader range of assets, including real estate, patents, royalties, and other property in addition to financial instruments. UTMA accounts are available in most states and offer more flexibility for families with non-standard assets to transfer.

For most Muslim families looking to invest in a halal equity or ETF portfolio on behalf of a child, a UGMA account is the most straightforward starting point.

Why Muslim Parents Invest for Their Children

The goals that motivate parents to open custodial accounts are consistent across most families - and they all trace back to the desire to give a child options and security that take years of compounding to build.

Education expenses are the most cited motivation. University costs in the U.S. have risen dramatically, and a family that begins investing for a newborn has 18 years to build a meaningful fund. A parent who starts at birth has a 6–8 year head start over one who begins when a child enters high school - and compounding makes that gap significant.

A first home is increasingly out of reach for young adults entering the workforce in high-cost U.S. cities1. A custodial account that a child receives at 21 with $80,000–$100,000 in it can serve as a down payment fund for a halal home purchase - a financial advantage most of their peers won't have.

Future financial security - the general principle that your child should begin adulthood with assets rather than debts - is a powerful motivation on its own, even without a specific goal attached.

Generational wealth building sits at the foundation of all of the above. Muslim families that invest intentionally across generations compound their financial and values legacy simultaneously. The child who grows up watching their custodial account and understanding what it represents will be better prepared to manage their own wealth responsibly when the time comes.

How Custodial Accounts Work in the U.S.

Opening a UGMA or UTMA account is straightforward - most major brokerage platforms offer them with no minimum investment and no contribution limits. You provide your information as the custodian and the child's information as the beneficiary, fund the account, and begin investing.

Contribution flexibility is one of the key advantages: there are no annual limits on how much you can contribute (though gifts above the annual gift tax exclusion - $19,000 per person in 20262 - may have gift tax implications). Contributions can be made by parents, grandparents, aunts, uncles, or any other adult.

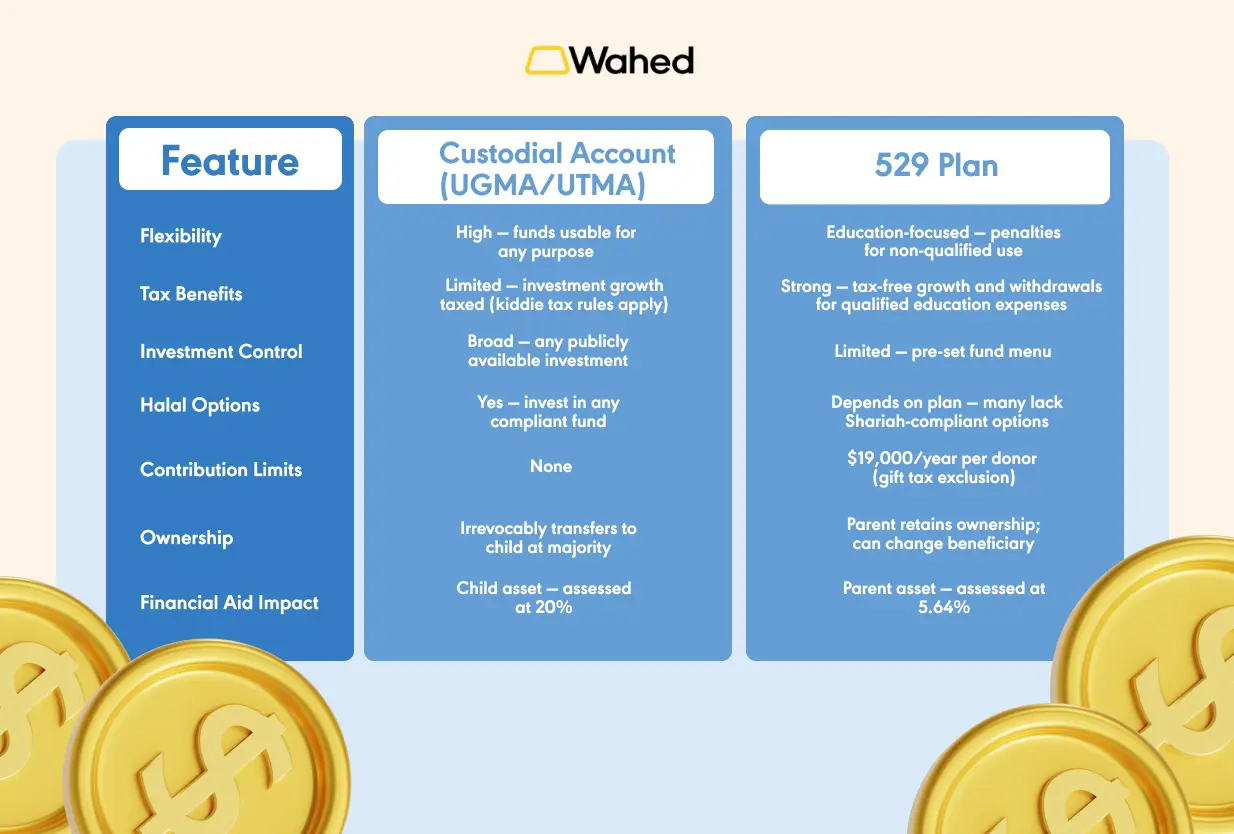

Investment options are broad - the same range available in any brokerage account: individual stocks, ETFs, mutual funds, and in some cases other asset classes. This is precisely what makes custodial accounts attractive for Muslim parents seeking halal investment options in the U.S. — you are not restricted to a limited fund menu the way you might be in a 529 plan.

Ownership and control shift automatically at the age of majority. Until that point, the custodian directs all investment decisions. After transfer, the child is under no obligation to use the funds for any particular purpose - they own the account fully and can use it however they choose.

Tax treatment: Investment income in a custodial account is subject to the "kiddie tax" rules — unearned income above a modest threshold (currently $2,700) is taxed at the parent's marginal rate rather than the child's lower rate, for children under 19 (or under 24 if full-time students). This reduces but doesn't eliminate the tax efficiency of the structure.

Are Custodial Investment Accounts Halal?

Yes, with the standard caveat that applies to all investment accounts: the account structure itself is neutral. Compliance is entirely determined by what you invest in, not the account type.

A UGMA account invested in Shariah-screened equities and halal ETFs is fully permissible - it is simply a legal container holding compliant investments. The same account invested in a conventional S&P 500 index fund (which includes banks, alcohol companies, and interest-bearing instruments) would not be compliant.

For Muslim parents, the practical requirement is the same as for their own portfolios: select investments that pass Shariah screening - sector exclusions for prohibited industries and financial ratio thresholds for debt and interest income. The good news is that the flexibility of UGMA and UTMA accounts means you can invest in any Shariah-compliant equity, ETF, or fund without restriction. This is a structural advantage over 529 plans, where investment options are limited to a predetermined fund menu that may not include compliant choices.

Custodial Accounts vs 529 Plans

Both custodial accounts and 529 education savings plans are commonly used by US parents to invest for children. The right choice depends on your goals, flexibility requirements, and tax situation.

The key trade-off is tax efficiency versus flexibility. A 529 plan offers meaningful tax benefits specifically for education expenses, but the investment menu is restricted and Shariah-compliant options are limited in most state plans. A custodial account offers broader investment freedom and halal flexibility at the cost of less favourable tax treatment and the permanence of asset transfer.

For Muslim families primarily focused on education funding and comfortable with conventional 529 fund menus, a 529 may still be worth considering for its tax advantages. For families who want full halal investment control and flexibility over how funds are eventually used, a custodial UGMA account is the more appropriate structure.

Benefits of Opening a Custodial Investment Account

Start Compounding Early. The most powerful argument for custodial accounts is also the simplest: time. A child born today has 18 years of compounding ahead before they reach adulthood - a runway that most adults would give a great deal to have again. Money invested when a child is born has the opportunity to compound for nearly two decades before it's needed. Starting at birth rather than at age 10 can more than double the terminal value of a consistent monthly contribution at typical long-term return rates.

Build Generational Wealth. A custodial account is the first step in teaching a family to think across generations rather than within a single lifetime. The child who receives a well-invested custodial account at 21 - and understands why and how it was built - is more likely to continue the practice for their own children. Generational wealth is built one compounding period at a time, and the families who start early build the habits and the capital that compound forward. For a broader framework on how this fits into a family's overall financial strategy, see our guide on the new Islamic year financial checklist for Muslim families.

Teach Financial Responsibility. A custodial account is not just a financial asset - it's a teaching tool. As children grow older, involving them in watching the account, understanding what investments are held and why, and seeing the compounding effect over time builds financial literacy in a way that no classroom lesson can match. A teenager who has watched their portfolio grow for a decade understands compounding viscerally, not abstractly.

Potential Drawbacks Parents Should Consider

Assets irrevocably belong to the child. Once transferred to a custodial account, funds legally belong to the minor and cannot be reclaimed. When the child reaches majority, they own and control the account entirely — regardless of whether you agree with how they choose to use it. Parents who are concerned about this should think carefully about how much to place in a custodial account versus retaining in their own name for the child's benefit.

Impact on financial aid eligibility. Custodial accounts are treated as student assets in financial aid calculations, assessed at 20%3 of value in determining Expected Family Contribution - significantly higher than the 5.64%4 rate applied to parental assets. For families expecting their child to apply for need-based financial aid, this can meaningfully affect eligibility.

Limited tax efficiency. Unlike a 529, investment gains in a custodial account don't grow tax-free. The kiddie tax rules mean that significant unearned income is taxed at the parent's rate. For larger balances, this should be factored into the overall decision.

How Much Should Parents Invest for Their Children?

The consistent message from long-term financial planning is that contribution amount matters less than starting early and investing regularly. The following table illustrates what different monthly contribution levels can grow to over 18 years at a 7% average annual return - consistent with long-term halal equity portfolio performance:

*For illustrative purpose only as rates of return will vary over time. Does not represent a real investment.

These figures assume consistent monthly contributions from birth to age 18. The takeaway is not that $250/month is always better than $50/month - it's that even a modest $50/month, maintained consistently, builds a meaningful foundation. Many Muslim families find that starting small and increasing contributions as income grows is the most sustainable approach.

The practical advice: open the account, set up a recurring monthly transfer at whatever level is realistic today, and increase it annually as your income allows. Automation removes the monthly decision - and consistent contributions across market cycles are what build long-term wealth.

For context on where idle cash should be held while deciding on an investment level, see our guide on can you earn halal returns?

What Investments Might Be Appropriate?

The brief here is to focus on concepts rather than specific product recommendations. Three categories are well-suited to a long-term custodial account for a child.

Diversified Halal Portfolios spread the child's capital across multiple Shariah-compliant asset classes - equities, sukuk, real estate exposure - in proportions appropriate for a long investment horizon. Because the time horizon is typically 15–18 years, a growth-oriented allocation makes sense in the early years, shifting gradually toward a more balanced approach as the target date approaches. For a framework on how to think about allocation across asset classes, see our halal portfolio diversification strategy.

Shariah-Compliant ETFs offer broad, low-cost exposure to screened halal equities within a single instrument. They are liquid, transparent, and require no per-stock research from the parent. A Shariah-certified ETF that tracks a recognised Islamic equity index is a practical core holding for most custodial accounts.

Long-Term Growth Investments in individual Shariah-compliant companies - for parents who are engaged investors and willing to conduct stock-level screening - can complement ETF holdings and provide the child with a concrete connection to specific businesses they understand. As the child grows older and begins to understand the portfolio, individual stock holdings in companies they can relate to (technology, healthcare, consumer goods) can be a particularly effective teaching tool.

Investing in Your Child's Future the Halal Way

The head start you give your child is not just financial - it's formational. A child who grows up with a portfolio invested in their name, built with intention and reviewed with care, learns something about discipline, patience, and values that no curriculum can teach.

The right time to open a custodial account is when your own financial foundation is stable - emergency fund in place, retirement contributions funded, high-cost debt addressed. When those boxes are checked, the next step is building for the generation that comes after you.

Sources:

1 The Guardian, June 18, 2026

2 IRS May 26, 2026

3 Federal Student Aid, Nov 20, 2025

4 Reddit, Jan 2026

Disclaimer:

Wahed Invest LLC (Wahed) is a U.S. Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only. Wahed does not provide tax, legal or accounting advice.