Key Takeaways:

You already invest. Maybe you hold a few Shariah screened stocks, a halal ETF, some cash in a savings account, and a retirement account at work. The harder question is whether it is actually diversified. A halal portfolio can pass every screening test and still be too concentrated in technology, too dependent on the U.S. market, too equity heavy for your time horizon, or holding too much cash for goals decades away.

This article walks through a practical framework for halal portfolio diversification: what diversification actually means, which asset classes are signified as halal, how to understand them, and how to keep a Shariah compliant portfolio aligned with your goals. Mainly, it provides a portfolio diversification consideration for Muslim investors in the U.S. who have moved past the question of whether to invest and now require structure.

What Is Portfolio Diversification?

Portfolio diversification means spreading investments across different assets, sectors, geographies, and risk profiles so no single weak area dominates the portfolio. The point is not to own many things, but to own things that behave differently from each other. For example, owning multiple technology stocks does not necessarily make a portfolio diversified. The stocks sit in the same sector, respond to the same forces, and tend to fall together. Real diversification reduces single company risk, single sector risk, geography risk, and liquidity risk. It supports long term stability without eliminating market risk.

For Muslim investors, diversification also has to be Shariah compliant. A portfolio that diversifies into conventional bonds or interest bearing income products may look balanced on paper, but it is not a Shariah compliant portfolio. A portfolio that holds only a handful of Shariah screened stocks is the opposite problem: halal, but concentrated. A more structured halal investment portfolio typically combines compliant U.S. equities, international equities, real asset exposure, commodities where appropriate, and non-interest based liquidity.

Why Diversification Matters in Halal Investing

Shariah screening removes conventional banks, conventional bonds, alcohol, gambling, tobacco, weapons, adult entertainment, and companies carrying excessive interest bearing debt. The investable set tilts toward sectors that pass screening more easily, such as technology, healthcare, industrials, and consumer businesses. Without an allocation framework, halal portfolios can become unintentionally concentrated in whatever happens to pass the screen.

A smaller universe does not eliminate diversification. It means Shariah compliant diversification has to be more intentional. Investors cannot simply buy "what is halal" and assume the result is balanced. They have to think about sector spread, geography, risk levels, and time horizon, and revisit that thinking as holdings evolve.

It also helps to be honest about performance. Shariah compliant investing performs differently, not necessarily worse. Some periods favor the sectors that dominate halal portfolios, particularly technology and healthcare. Other periods favor the financial and energy sectors that screening tends to exclude. The goal is not to replicate a conventional portfolio. It is to build a compliant portfolio that manages risk intelligently within Islamic finance principles. For a deeper structural comparison, see our blog on Halal vs Conventional Investing in the U.S.

What Asset Classes Are Halal?

No asset class is automatically halal in every form. Structure, financing, income source, and underlying holdings all matter. The label tells you very little on its own.

Equities (or Stocks)

Shares of companies can be halal when the business activity is permissible and the financial structure passes screening. Two layers apply: business activity screening removes companies whose main revenue comes from prohibited industries, and financial ratio screening removes companies carrying too much interest bearing debt or generating too much interest income. Owning individual halal stocks gives direct visibility, but it creates research burden and concentration risk. Pure technology picks is not a diversified portfolio.

ETFs

Halal ETFs provide diversified exposure to a basket of screened companies in a single purchase. They reduce single stock risk and outsource screening to a fund provider with Shariah oversight. A single halal ETF, however, may concentrate in one country, sector, or market cap range, and two halal ETFs that look different on the label can hold many of the same companies underneath. Investors should know what each fund owns and what role it plays in the broader allocation.

Real Assets

Real assets include real estate, commodities, and physical infrastructure exposure. Their return drivers differ from public equities, which is what makes them useful for diversification. Real estate can offer income opportunities and inflation sensitivity. Commodities such as gold can act as a diversifier, though they are volatile and should not be treated as guaranteed downside protection. Halal real estate sounds simple, but financing structure, leverage, tenant activity, and income source all matter. Many conventional REITs typically hold significant interest bearing debt or earn income from tenants whose primary business is non compliant. Our article on is real estate investing halal in the U.S. walks through the practical considerations.

Cash Allocations

Cash supports liquidity and stability, but Muslim investors should be cautious with conventional interest bearing cash products. Cash is not a growth engine. Holding too much over long periods creates inflation risk, because the purchasing power of idle cash erodes year after year. Holding too little can force an investor to sell long term holdings during a downturn to cover an unplanned expense. The right level depends on goals, income stability, and how the rest of the portfolio is constructed.

Core Principles of a Diversified Halal Portfolio

Six principles guide most disciplined halal asset allocation. They work as a checklist, not a formula.

1. Minimize concentration risk. A portfolio should not depend too heavily on one company, one ETF, one employer stock, one sector, one country, or one asset class. Single positions, even excellent ones, may produce outcomes the broader market does not.

2. Diversify across sectors. Because screening removes financials and parts of other sectors, halal investors should check where the remaining exposure is concentrated. Technology and healthcare are typically overrepresented after screening.

3. Diversify across geographies. A portfolio limited to U.S. equities misses international exposure. Global diversification spreads economic cycles, currencies, and regional market risks, though international holdings still require their own Shariah screening.

4. Balance risk levels. Aggressive investors may hold more equities. Conservative investors may lean toward liquidity, sukuk where appropriate, and lower volatility holdings. The right balance reflects the investor's situation, not a target on a chart.

5. Align allocation with time horizon. Money needed within two years should not sit in the same allocation as money intended for retirement in twenty five years.

6. Keep compliance active. Halal compliance is not a one time decision. Companies change. Debt levels rise, business activities expand, revenue mixes shift, and screening outcomes can flip. A Shariah compliant portfolio needs periodic review.

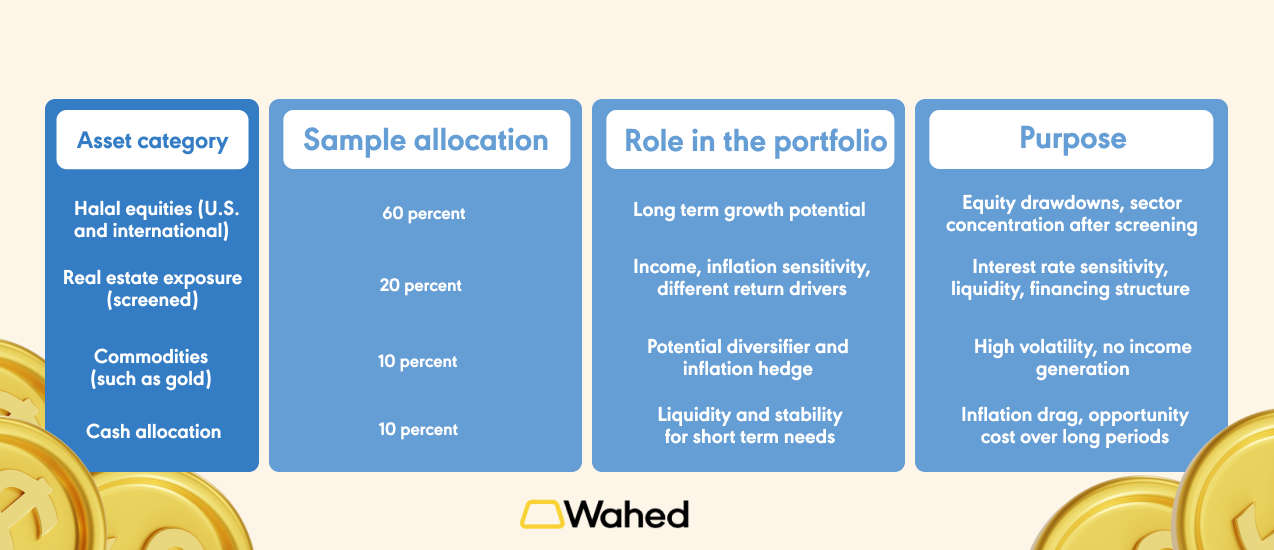

Example Halal Portfolio Allocation

The allocation below is a hypothetical illustration, not a recommendation. It shows one way a balanced Shariah compliant portfolio might be structured. Real portfolios should reflect each investor's goals, time horizon, and risk tolerance rather than a generic template.

A few caveats. A twenty five year old saving for retirement may reasonably hold a higher equity weight and skip cash beyond an emergency fund. An investor five years from retirement may want more stability. The right halal asset allocation is the one the investor can hold through difficult markets without selling at the wrong moment.

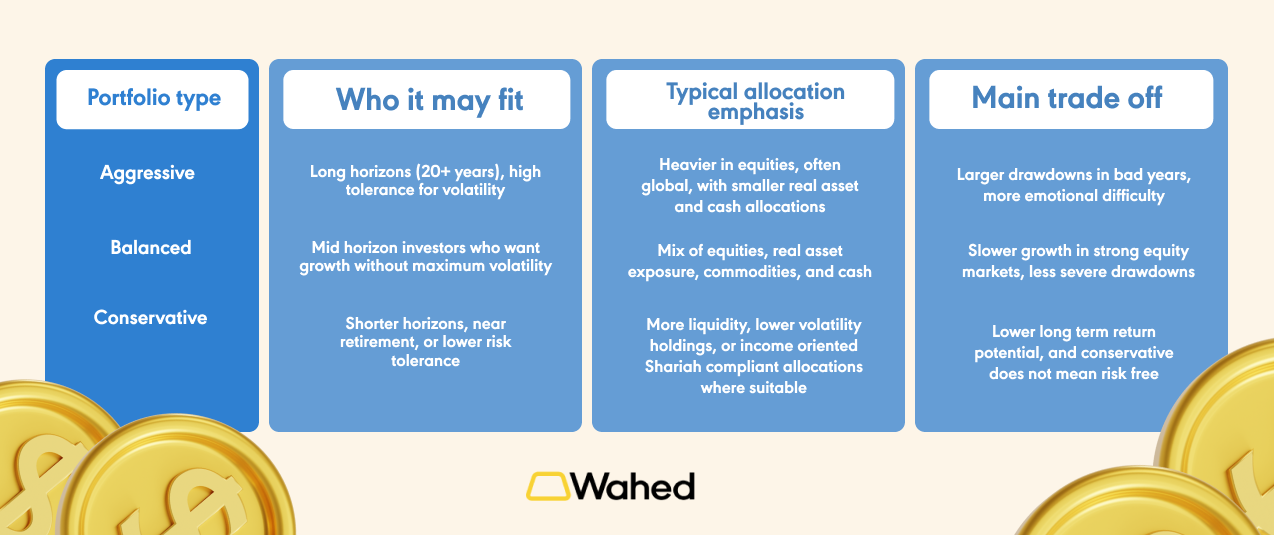

Aggressive vs Balanced vs Conservative Halal Portfolios

The same halal asset classes can be combined very differently depending on goals and risk tolerance.

Wahed Robo Advisor is built around this principle. Investors specify a goal and risk tolerance, and the portfolio is constructed and maintained around that profile rather than reassembled each quarter.

How to Diversify Without Overcomplicating

Diversification is not a numbers game. Owning eighty investments is not better than owning twelve well chosen ones if the eighty investments overlap. Investors may end up with several halal ETFs that own substantially the same companies, which feels diversified but is not.

A simple framework helps. Core holdings should do most of the portfolio's work, typically through broad halal ETFs or a managed halal portfolio covering compliant asset classes in one structure. Satellite holdings should be limited and intentional: a specific real estate vehicle, a commodity allocation, or a higher conviction equity position, added because they play a defined role. Cash should serve liquidity needs, not act as a permanent default. Real assets should serve diversification, not excitement.

The DIY question deserves an honest answer. DIY halal investing gives the investor control over every screen, allocation, and rebalance, which is genuinely valuable for those who enjoy the work. It also requires time, ongoing compliance checks, and the discipline to rebalance rather than chase performance. Managed halal portfolios remove most of that burden for investors who would rather not turn portfolio management into a second job. Explore the difference between active and passive investment through a partner.

Build a Diversified Halal Portfolio Today

For investors who want professional portfolio construction and ongoing management without taking on the screening and rebalancing work themselves, Wahed's managed halal portfolios are designed to help Muslim investors build diversified portfolios aligned with their goals and risk tolerance. For a broader orientation, our guide to halal investing in the U.S. is a useful next stop.

Disclaimer:

Risk Disclosure: For U.S. audience. Wahed Invest LLC (Wahed) is a U.S. Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.