Key Takeaways:

If you're already investing through ETFs - or planning to - the question isn't whether ETFs can be halal. They can. The question is knowing precisely what determines compliance, so you're not relying on a label or a fund name to make that call for you.

This article covers the full framework: the Islamic finance principles behind halal ETF screening, the specific financial ratios used, how Shariah scholars certify funds, and what a compliant ETF portfolio actually looks like compared to a conventional one.

What Is an ETF?

An Exchange-Traded Fund (ETF) is a basket of securities - stocks, bonds, commodities, or a mix - that trades on a public exchange like a single stock. Instead of buying shares in one company, you buy a single ETF unit that gives you proportional exposure to everything inside it.

ETFs have become the dominant vehicle for individual investors because they combine three things that are otherwise hard to get simultaneously: diversification, low cost, and liquidity. A single S&P 500 ETF, for example, gives you exposure to 500 companies across every major sector of the U.S. economy with a management fee often below 0.05%.

That combination makes ETFs highly attractive for Muslim investors too - in principle. The challenge is that most mainstream ETFs, including the most popular S&P 500 trackers, contain companies and asset classes that are not Shariah-compliant. The ETF structure itself is neutral, but what's inside it is not always halal.

Are ETFs Halal in Islam?

ETFs are not inherently halal or haram. An ETF is an actual investment (a security), whereas an IRA or a brokerage account is simply an account used to hold investments. At the same time, an ETF can be thought of as a legal structure - a container that holds a basket of underlying assets. Their permissibility depends on what the ETF invests in. In other words, compliance is determined by the nature of the underlying holdings and activities of the companies or instruments held within the ETF.

A Shariah-compliant ETF holds only companies that have been screened against Islamic finance principles. A conventional ETF holds whatever the index it tracks including - banks, alcohol companies, bond funds, and all.

The Islamic finance framework that governs halal ETF compliance is built on two foundational principles: avoiding riba (interest-based returns) and avoiding investment in industries that cause harm or engage in impermissible activities. A halal ETF must pass on both dimensions - not just one.

Key Principles of Halal Investing

Before getting into the mechanics of screening, it helps to understand what the screening is trying to achieve.

Avoiding riba (interest). Any financial return generated through lending at interest is prohibited. This means bond ETFs - corporate bond funds, government bond funds, aggregate bond index funds - are categorically not halal. The same applies to ETFs with significant bond allocations, including most target-date retirement funds. A halal ETF is equity-based, generating returns through business ownership and profit-sharing rather than interest.

Avoiding prohibited industries. Companies whose primary business involves Shariah-prohibited activities cannot be held in a Shariah-compliant portfolio, regardless of their financial metrics. This isn't a marginal concern - mainstream index ETFs routinely include these companies as significant holdings.

Investing in ethical businesses. The positive corollary: halal investing directs capital toward companies engaged in genuine productive activity that benefits society - technology, healthcare, consumer goods, real assets - businesses you can hold with confidence.

Industries That Make an ETF Shariah non compliant

The sector exclusions in Shariah-compliant ETFs follow a consistent ethical logic. Any ETF holding significant exposure to the following industries is not halal:

Alcohol. Companies involved in producing, distributing, or selling alcoholic beverages are excluded. This includes brewers, distillers, wine producers, and retailers where alcohol forms a meaningful share of revenue. A company like a supermarket chain where alcohol is a small fraction of total sales may be assessed differently - which is where the revenue threshold test (discussed below) becomes important.

Gambling. Casinos, online betting platforms, lottery operators, and sports gambling companies derive their income from maysir - acquiring wealth through chance at others' expense. These are excluded outright.

Conventional banking. Traditional banks operate on an interest spread - borrowing at one rate, lending at a higher rate. This interest-based model constitutes riba, making virtually all major U.S. commercial and investment banks non-compliant. This is the largest single sector exclusion in a typical halal ETF and explains why halal portfolios have significantly lower financial sector exposure than standard index funds.

Adult entertainment. Any company whose primary or significant business involves adult content is excluded.

Weapons and defence. Companies whose revenue is materially or primarily derived from weapons systems manufacturing - particularly those used in direct combat applications - are excluded. This does not necessarily include all aerospace or defence contractors, which may have significant civilian operations; the revenue breakdown determines compliance.

Tobacco. Excluded on grounds of demonstrable harm - a principle that aligns with an increasing number of ethical investing frameworks globally.

The rationale across all categories is coherent: halal investing will not generate returns from businesses whose model depends on harming people, exploiting weakness, or operating through impermissible financial mechanisms.

Financial Ratio Screening

Sector exclusion handles the obvious cases. Financial ratio screening handles the nuanced ones - companies in otherwise permissible industries whose financial structure involves excessive interest-based debt or generates meaningful income through non-compliant activities.

This is the layer that most generic "ethical" funds skip, and it's where Shariah screening is genuinely distinct.

Three standard financial ratio tests:

1. Interest-bearing debt ratio. A company's total interest-bearing debt (loans, bonds issued, credit facilities) must be typically below 33% of its total assets¹ (or total market capitalisation, depending on the methodology). A technology company that has taken on significant leveraged debt to fund acquisitions, for example, may fail this test even if its core business is permissible.

Why it matters: A company highly dependent on interest-based financing is essentially extracting value through riba even if it's in a halal industry. The investor's returns would be partially generated through that mechanism.

2. Cash / interest-bearing securities ratio. Interest income earned by the company (from cash deposits, financial investments, or lending activities) must be typically below 33% of total assets. Many large tech and consumer companies hold substantial cash reserves generating interest - this test ensures that income stream doesn't become a meaningful component of the business.

3. Non-compliant income threshold. Revenue from any prohibited activity - even if not the company's primary business - must typically fall below 5% of total revenue². A diversified retailer that sells alcohol but derives less than 5% of revenue from it may still pass, subject to the requirement for income purification (disposing of the proportional impermissible income to charity).

Together, these three tests create a meaningful financial filter that goes beyond simply checking whether a company is in a permissible industry.

How Shariah Scholars Certify Halal ETFs

The certification process for a genuinely Shariah-compliant ETF involves independent oversight at every stage - not self-certification by the fund manager.

Shariah supervisory board. A qualified Shariah board consists of Islamic finance scholars with expertise in both fiqh (Islamic jurisprudence) and modern financial instruments. They are independent of the fund manager, which is critical - they have no commercial incentive to approve holdings that don't meet the standard.

Screening methodology review. The board reviews and formally approves the screening methodology before the fund launches - establishing the specific criteria for sector exclusions, financial ratio thresholds, and edge case handling. This methodology is documented and disclosed.

Initial fund screening. Every holding in the fund is assessed against the approved methodology before inclusion. For ETFs tracking a Shariah-screened index, the index provider conducts this screening; the Shariah board validates the process.

Ongoing monitoring and rebalancing. Company financials change. A business that passed the debt ratio test last year may fail it this year after a leveraged acquisition. Shariah-compliant funds conduct periodic re-screening - typically quarterly or annually - and rebalance to remove holdings that fall out of compliance.

Purification guidance. Where a holding generates a small amount of non-compliant income (within the 5% threshold), the board calculates the purification amount - the proportion of returns the investor should dispose of that amount to charity to cleanse that income. This reflects the precision of the scholarly approach: compliance is not binary in every case, and the framework has mechanisms for managing grey areas responsibly.

This is what distinguishes a formally certified Shariah-compliant ETF from a fund that simply avoids the most obvious haram sectors without the underlying financial ratio analysis and independent oversight.

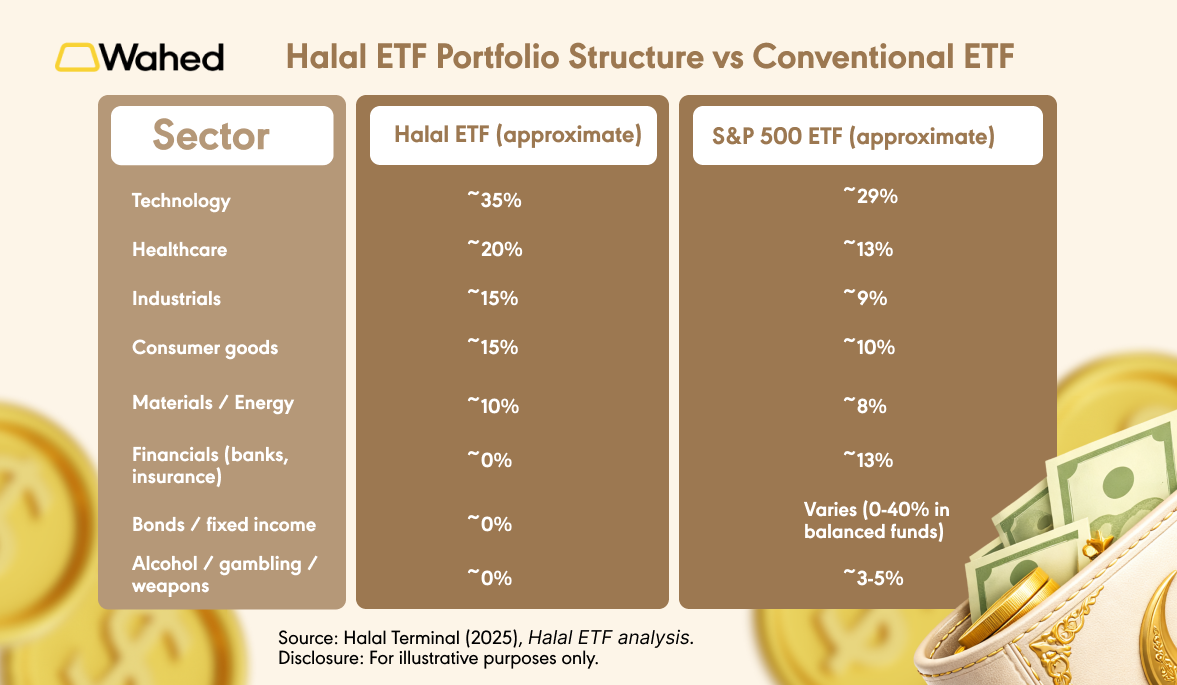

Example: Halal ETF Portfolio Structure vs Conventional ETF

To see the difference concretely, compare the sector composition of a Shariah-compliant equity ETF against a standard S&P 500 ETF³:

The most visible differences: zero financial sector exposure (due to riba exclusion of conventional banks) and zero bond allocation (interest-based instruments). This results in a halal ETF that is more concentrated in technology and healthcare relative to the broad market - which has generally been neutral to positive over recent market cycles, though past sector performance does not predict future results.

The halal ETF universe is smaller - you're investing in a screened subset of the market. But it remains genuinely diversified across hundreds of companies, multiple sectors, and - in global halal ETFs - multiple geographies and market capitalisations.

Investing the Halal Way

For Muslim investors, the goal is not to avoid the market - it's to participate in it fully while ensuring that every holding reflects your values and your obligations.

Halal ETFs make that practical. They provide the diversification, low-cost structure, and accessibility of conventional ETFs, with the Shariah compliance framework and independent oversight that removes the burden of individual stock screening from each investor.

Sources:

¹ Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) (2017), Shariah standards. https://aaoifi.com/shariaa-standards/?lang=en

² Institute of Halal Investing (2025), Understanding Shariah screening ratios: How halal stocks are really evaluated. https://www.instituteofhalalinvesting.org/single-post/understanding-shariah-screening-ratios-how-halal-stocks-are-really-evaluated

³ Halal Terminal (2025), Halal ETF analysis. https://www.halalterminal.com/research/halal-etf-analysis

⁴ Charles Schwab (2025), ETFs: How much do they really cost? https://www.schwab.com/learn/story/etfs-how-much-do-they-really-cost

Disclaimer:

This article is for educational purposes only and does not constitute religious, financial, or legal advice. Investing involves risk, including the loss of principal. This is not a recommendation to buy or sell any specific security. We recommend consulting a qualified Islamic scholar for guidance on your specific situation. Past performance is not indicative of future results. Wahed Invest LLC is a registered investment adviser with the SEC.