Key Takeaways:

You already think about where your money goes. Maybe you hold an ESG ETF in a brokerage account, a sustainability themed fund in your 401(k), or an index fund marketed as values aligned. The fund avoids tobacco, scores well on governance, and feels more thoughtful than a standard S&P 500 holding. The harder question, the one most ESG marketing does not answer, is whether any of that makes the fund halal. Avoiding fossil fuels is not avoiding riba, and a strong ESG rating is not Shariah oversight.

This article works through the actual difference between halal investing vs ethical investing in the ESG sense: what each framework means, where they overlap, where they part ways, and how a Muslim investor in the U.S. should choose. Especially for those who want a clear answer to a specific question, which is whether ESG funds halal or haram is even the right framing, and what to do next when the answer is "it depends on what the fund actually holds."

What Is ESG Investing?

ESG stands for Environmental, Social, and Governance. As a framework, it evaluates companies on factors such as climate impact, labor practices, supply chains, board structure, executive compensation, and community impact. The idea is that companies which manage these issues well may also manage long term business risk better.

ESG funds apply these ideas in very different ways. Some use exclusionary screens that remove industries like tobacco or controversial weapons. Some rely on third party ratings. Some apply a best in class approach. Some integrate ESG analysis without removing many companies at all. Two providers can rate the same company very differently, because methodologies are not standardized.

A fund labeled "ESG" or "sustainable" tells you ESG factors were considered. It does not tell you the fund meets any single ethical standard, and it does not tell you the fund meets Islamic finance standards.

What Is Halal Investing?

Halal investing, also commonly referred to as Shariah-compliant investing, applies Islamic finance principles to how money is invested. The goal is long term wealth building; the constraint is what that wealth is built through.

Three core rules define the framework. The first is avoiding riba, meaning interest based lending or interest based returns. This is the most structural difference from conventional and most ESG investing, because it categorically excludes conventional bonds and the income conventional banks generate from spread lending. The second is avoiding haram industries: alcohol, gambling, tobacco, adult entertainment, weapons, pork related businesses, and conventional financial services. The third is preferring businesses with permissible core activities while avoiding excessive speculation.

Halal investing adds a layer ESG typically does not: financial ratio screening. A company in a permissible industry can still fail if its balance sheet relies too heavily on interest bearing debt or generates significant interest income. A credible halal product is overseen by qualified scholars who validate the methodology and review holdings on an ongoing basis. For a fuller walkthrough, see our guide to halal investing in the U.S..

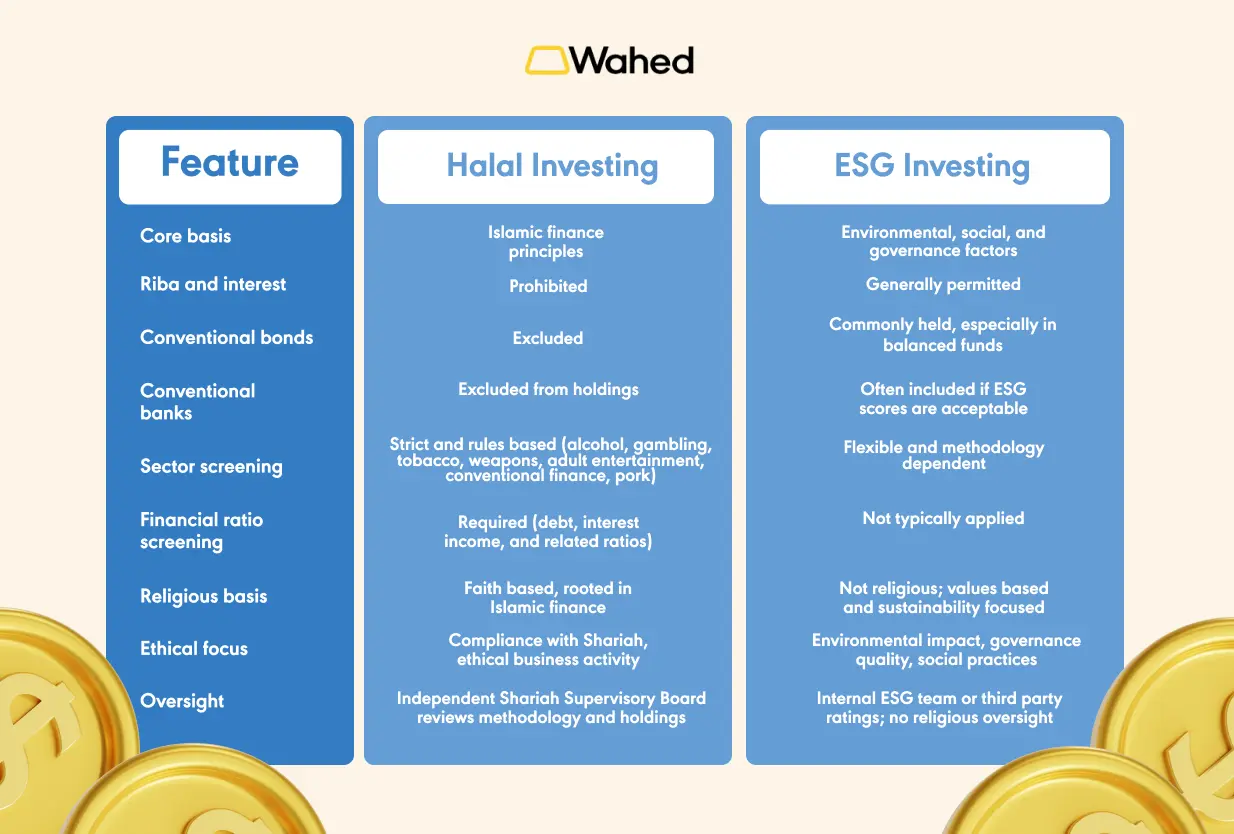

Key Differences Between Halal and ESG Investing

The clearest way to see the gap in Shariah vs ESG investing is side by side.

The most important takeaway sits beneath the rows. ESG asks whether a company is acceptable on environmental, social, and governance factors. Halal investing asks whether the investment is permissible under Islamic finance principles. Related questions, but not the same question. A company can score well on ESG and still fail Shariah screening because of its interest bearing debt, its income mix, or the sector it operates in.

Do ESG Funds Meet Halal Requirements?

The short answer is that ESG funds do not automatically meet halal requirements. Most do not by default, though it depends on the specific fund.

An ESG fund may still include conventional banks (which often score well on governance), companies with debt levels that fail Shariah financial ratio screening, conventional bonds or interest based investments in any balanced strategy, and some haram industries its methodology does not exclude. It may evaluate climate risk or governance quality without applying a riba screen. The ESG label itself does not imply independent Shariah oversight.

A Muslim investor evaluating any ESG product has practical work to do: review the holdings, the screening methodology, the revenue mix, the presence of a Shariah board, and whether the fund applies a recognized Islamic finance screening standard. Our piece on what makes an ETF halal walks through these checks in detail.

Where Halal and ESG Overlap

The overlap is real. Both approaches reject the idea that investing is only about return. Both consider harm, ethics, and social impact. Tobacco, controversial weapons, gambling, and companies with severe governance failings can fail either screen. Both appeal to investors who do not want to profit from harmful activities.

The overlap is not complete. ESG can be broader in environmental and governance areas, including emissions targets, board diversity, and shareholder rights that halal screening does not specifically address. Halal investing is stricter and more specific where Islamic finance principles apply, particularly around riba, haram revenue, conventional financial services, and financial ratio thresholds. A Muslim investor who cares about both can look for products that apply both frameworks, but halal compliance should not be assumed from an ESG label.

Which Approach Is Better for Muslim Investors?

The right answer depends on what the investor is trying to do. If the primary goal is broad values based investing without a religious framework, ESG may be useful. If the primary goal is Islamic compliance, halal investing is the more directly relevant framework. If the investor wants both, start with Shariah screening and consider ESG factors as an additional layer, rather than starting with ESG and hoping it covers halal.

For Muslim investors who want their portfolio to comply with Islamic finance principles, ESG alone is not enough. Decision factors include the investment objective, the religious requirement, transparency of holdings, the screening methodology, riba and bond exposure, haram industry exposure, Shariah oversight, fees, diversification, and risk tolerance.

There is a fair "why not just buy an ESG ETF through other platforms that offer ESG ETFs?" objection. The honest answer is that the platform and fund label do not determine halal status. The underlying holdings, income sources, debt levels, and screening methodology do.

Example: ESG Fund vs Halal Portfolio

Imagine a U.S. Muslim professional with $50,000 invested for long term growth, weighing a broad ESG ETF against a managed halal portfolio.

The ESG fund screens for environmental practices, labor issues, governance, and certain controversial industries. It may reduce exposure to fossil fuels or tobacco and exclude controversial weapons, while including conventional financial companies, which often score well on governance. If the fund holds bonds, those bonds generate interest income. Its income mix and debt levels are not screened against Islamic finance principles.

The halal portfolio is built differently from the start. It applies Shariah screens to avoid riba, haram industries, and non compliant financial structures, and may include Shariah screened U.S. and international equities, halal ETFs, sukuk as an income oriented allocation, and other compliant holdings depending on goals and risk tolerance. The ESG fund starts with values and sustainability criteria; the halal portfolio starts with permissibility under Shariah and builds within that framework.

Common Mistakes Muslim Investors Make When Comparing ESG and Halal

The most common mistake is assuming ESG means halal. ESG considers environmental, social, and governance factors, not riba or financial ratios. Verify the screens, not the label. Closely related mistakes: assuming every ethical fund avoids riba (many include bonds or interest income from cash), ignoring the bond allocation (a balanced ESG fund may be 30 to 40 percent bonds, which are not Shariah compliant), and reading the fund name as if it were the methodology.

Other versions: assuming a retirement account is halal because the investor chose an ESG option within it (the wrapper is not the contents), confusing negative screening with Shariah screening (the financial ratio layer is missing), and assuming halal investing ignores environmental or social concerns (it has its own framework for considering harm).

How Wahed Helps Bridge the Gap

Many Muslim investors start with ESG because it feels closer to their values than a conventional index fund. ESG is usually not designed to answer the Shariah compliance question. Using it as a proxy leaves real gaps around riba, conventional financial services, and financial ratios. For Shariah compliance, the portfolio needs to be built on Islamic finance principles from the start.

This is the gap Wahed's managed halal portfolios are designed to fill. Wahed’s Robo Advisor matches investors with diversified portfolios based on goals and risk tolerance, using a Shariah compliant framework rather than an ESG one. The benefit is structure: less guesswork than comparing ESG funds manually, more discipline than buying halal stocks one at a time, more clarity than assuming a workplace ESG option is compliant. Investing involves risk, including possible loss of principal; Shariah compliance does not remove market risk.

Investing With Purpose and Principles

ESG investing has helped many investors think more carefully about what their money supports. For Muslim investors, the conversation goes further. The question is not only whether a company looks responsible on environmental, social, or governance metrics, but whether the investment is permissible under Islamic finance principles, which is a different test with different answers.

Start from Shariah and layer ESG considerations on top if they matter personally, rather than starting from ESG and hoping it covers halal.

Disclaimer:

Risk Disclosure: For U.S. audience. Wahed Invest LLC (Wahed) is a U.S. Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.