Key Takeaways:

If you've been keeping an eye on personal finance content over the past few years, high-yield savings accounts have been impossible to miss. With interest rates climbing to levels not seen in decades, HYSAs were suddenly offering 4%-5% APY¹ - and financial influencers were telling everyone to move their emergency fund immediately.

For many Muslim Americans, that advice came with a catch. Interest - in any form, earned or paid - sits at the heart of the riba prohibition in Islamic law. A savings account that generates returns specifically through interest raises a genuine compliance question, regardless of how attractive the rate looks on paper.

This article explains how HYSAs work, what Islamic finance principles apply to savings accounts, and what alternatives exist for Muslims in the U.S. who want their money to work for them without compromising on their deen.

What Is a High Yield Savings Account (HYSA)?

A high-yield savings account is a type of deposit account - typically offered by online banks or financial institutions - that pays a significantly higher interest rate than a standard savings account. Where a traditional bank savings account might pay 0.01%-0.5% APY², HYSAs routinely offer 4%-5% APY³ when market interest rates are elevated.

HYSAs work through the same basic mechanism as any bank deposit: you deposit money, the bank lends it out or invests it at a higher rate, and the bank pays you a portion of those returns as interest. The account balance is FDIC-insured up to $250,000⁴, making HYSAs a low-risk vehicle by conventional standards.

Their popularity is understandable. In a high-interest-rate environment, a $20,000 emergency fund sitting in a HYSA at 4.5% generates $900 in interest per year - compared to $10-$20 in a standard savings account. For savers focused on capital preservation and liquidity, the HYSA became the obvious choice for anyone not thinking about Shariah compliance.

What Is a Halal Savings Approach?

A halal savings approach refers to any method of storing and growing capital that avoids interest - either earned or paid. In practice for a Muslim saver in the U.S., this means keeping short-term savings in accounts or vehicles that don't generate riba, even when interest-bearing alternatives might offer higher nominal returns.

The Islamic finance framework that governs this isn't primarily about rates of return - it's about the mechanism through which returns are generated. Returns from Shariah-compliant ownership of productive assets (equity in a halal business, rental income from permissible property, profit-sharing arrangements) are generally permissible. Returns generated simply from the act of lending money at a fixed, predetermined rate - regardless of the underlying economic activity - are riba.

For savings specifically, the focus tends to be on capital preservation rather than aggressive growth. Emergency funds and short-term savings don't need to be high-yielding - they need to be accessible, stable, and halal. The appropriate ambition for a six-month emergency fund is not maximum return; it's keeping those funds available, low, and compliant. For a broader grounding in how Islamic finance principles shape financial decisions, our overview covers the foundational framework.

Why Interest (Riba) Is Prohibited in Islam

Riba is one of the most clearly and repeatedly prohibited acts in the Quran and Sunnah. The word translates roughly as "increase" or "excess" and refers specifically to the practice of charging or receiving a predetermined increase on a loan of money, regardless of economic outcomes.

The Islamic reasoning behind the prohibition operates on multiple levels. At the theological level, the Quran explicitly and repeatedly condemns riba and draws a sharp distinction between it and trade (Qur’an 2:275) - both generate returns, but only trade involves real risk, real effort, and genuine economic production. At the ethical level, interest is seen as exploitative - it enriches the lender regardless of whether the borrower succeeds or fails, concentrating wealth without contributing to productive activity.

The implication for savings accounts is direct. A HYSA pays you interest specifically because the bank is lending your money to others at a higher rate and keeping the spread. Your return - 4.5% APY - is treated as riba under Islamic finance principles: it is a predetermined, fixed increase on your deposited capital, regardless of what happens in the wider economy. Whether the bank uses your funds to make car loans, mortgages, or business loans, your return is fixed and guaranteed. That structure is precisely what Islamic finance prohibits.

Some scholars draw a distinction between paying riba (borrowing at interest) and receiving riba (earning interest), but the mainstream scholarly position across madhabs is that both are prohibited. For a comprehensive overview of where this ruling intersects with investment decisions, see our guide on halal vs conventional investing.

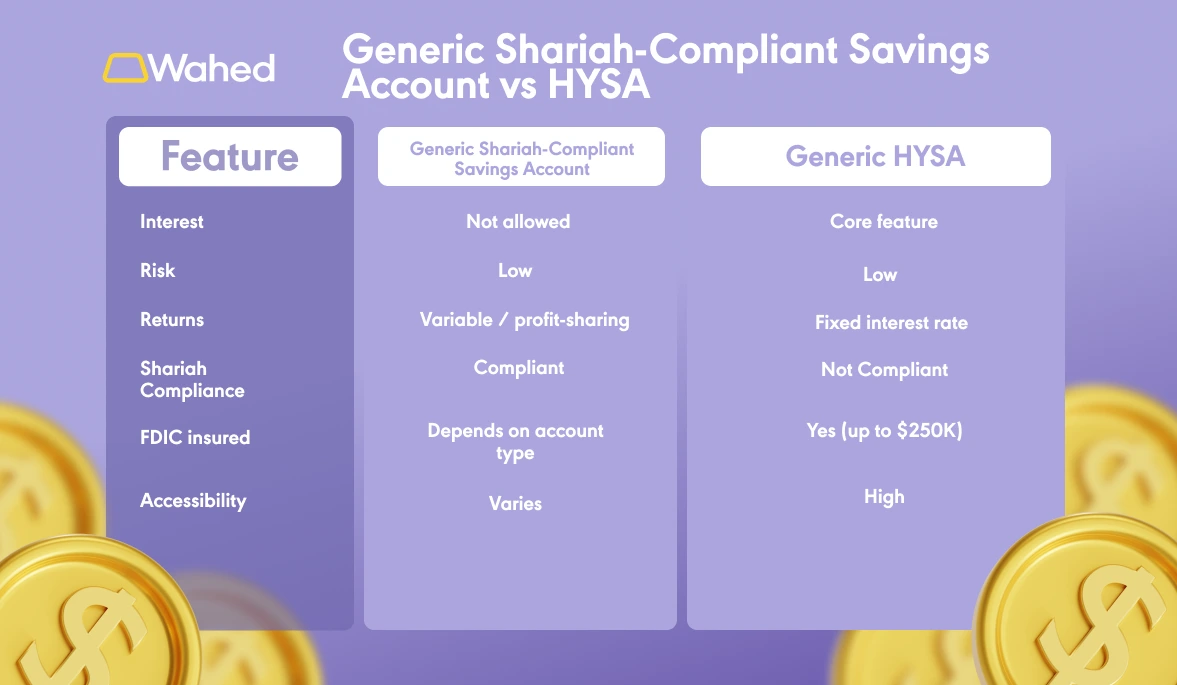

Key Differences: Generic Shariah-Compliant Savings Account vs HYSA

The table makes the core difference clear: it's not primarily about risk or accessibility - both approaches can preserve capital effectively. The defining distinction is whether the return mechanism involves interest. For a Muslim investor, that single row determines the compliance status of the account.

What Are the Alternatives to High Yield Savings Accounts?

The honest answer is that the U.S. banking infrastructure is not well-designed for Muslim savers seeking interest-free deposit products. Dedicated Islamic banking products are limited in the U.S. compared to markets like the UK, Malaysia, or the Gulf. But practical alternatives do exist, and Muslim savers increasingly have workable options.

Non-interest savings accounts. The most conservative approach is simply using a standard bank account that earns no interest - or opting out of interest crediting where the bank allows it. This preserves capital without generating any riba. The downside is obvious: your savings generate nothing. In a high-inflation environment, idle cash loses real purchasing power each year. This approach is appropriate for very short-term needs (money earmarked for an expense in the next 30-60 days) but becomes costly over longer periods.

Halal investment accounts for short-term capital. For savers with a 6-18 month horizon who want their capital working without riba, low-volatility halal investing options offer a middle path. Approved Shariah-compliant investment alternatives and lower-volatility screened portfolios are designed (or seek) to preserve capital while generating returns through permissible profit-sharing mechanisms rather than interest. The trade-off is some degree of market risk - these are not guaranteed-return vehicles, but for capital that doesn't need to be accessed for six months or more, this is a meaningful option. For context on how halal investing works across asset classes, our halal investing guide provides a comprehensive overview.

Short-term halal portfolios. A Shariah-compliant managed portfolio with a conservative risk profile can serve as an investment vehicle for Muslim savers who want their money productively deployed without interest. Returns vary with market conditions and are not guaranteed. But for medium-term savings (house down payment savings, emergency fund supplementation), this structure offers a halal-investing alternative to the HYSA for those who understand and accept that trade-off.

Should Muslims Keep Money in HYSA?

This is the practical question most Muslim Americans with a HYSA are wrestling with - and it deserves a direct, honest answer.

The mainstream scholarly view is that earning interest from a HYSA is not permissible under Islamic finance principles. The account is specifically designed to generate interest income, and that income is riba regardless of the saver's intention.

Some scholars have discussed nuance around necessity and the absence of genuine halal alternatives - arguing that if no compliant product is available, keeping money in a basic bank account without actively seeking interest may be permissible as a matter of necessity. But this is a position of last resort, not a general ruling endorsing HYSAs, and most scholars who hold this view would not extend it to actively choosing the highest-interest account available.

Practical considerations matter too. Many Muslim Americans are already holding savings in HYSAs - either because they opened them before their understanding of Islamic finance deepened, or because they were unaware of the riba concern. The constructive path is not guilt, but informed decision-making going forward: understand the alternatives, make a considered choice, and if interest has already been received, consult a scholar about purification (disposing of the interest income by giving it away without intending reward, which is a widely accepted approach for incidentally received riba).

The question of intent is real but not determinative. Keeping money in a HYSA knowing it earns interest, while intending to give the interest away, is treated differently by different scholars - some permit it as a form of purification practice, others advise simply moving to a compliant alternative once one is accessible. Consulting a qualified Islamic scholar for personal guidance is the right approach for those with specific circumstances.

Example: Saving vs Investing Halal

Consider two Muslim savers, each with $10,000 in short-term savings.

Saver A keeps her $10,000 in a HYSA at 4.5% APY. After one year she has $10,450 in interest income. She's aware of the riba concern but hasn't yet made the switch.

Saver B keeps $5,000 in a non-interest account as his liquid emergency fund and invests the remaining $5,000 in a Shariah-compliant conservative portfolio using Shariah-compliant screened investments. Over one year, at a modest 5% hypothetical return, his invested $5,000 grows to approximately $5,250. His total savings position: $10,250 - slightly below Saver A's nominal number, but structured to avoid riba.

Now extend the timeline to ten years, assuming Saver B continues to invest his medium-term savings in a halal portfolio and both savers reinvest their returns. At a hypothetical 7% average annual return* - consistent with long-term halal equity portfolios - Saver B's $5,000 invested portion grows to approximately $9,835 over a decade. More significantly, as he builds confidence in islamic investment in the U.S., he progressively moves his emergency fund top-up capital into productive halal vehicles rather than idle cash, accelerating growth across his whole savings picture.

The point isn't that halal investing always generates higher returns than a HYSA - it's that the compliance and the long-term wealth-building trajectory can both be served without choosing interest. For practical guidance on putting spare capital to work the halal way, see our article on how to invest your tax refund the halal way.

* For illustrative purposes only as rates of return fluctuate over time and unlike traditional savings accounts, investing involves risks including loss of principal. 7% hypothetical return shown is based on historical averages.

Start Building Halal Wealth

The HYSA question is ultimately a small piece of a larger picture. The real goal - for any Muslim building financial stability in the U.S. - is a holistic approach to money that aligns every financial decision with Islamic values: savings that don't earn riba, investments that are screened for compliance, and wealth that is built through productive, ethical means.

That picture is entirely achievable. The tools available for halal investing in the U.S. have expanded significantly in recent years - from Shariah-screened equity portfolios to professionally managed Shariah-compliant portfolios that handle compliance on your behalf. The path from a HYSA to a fully faith-aligned financial life doesn't need to happen overnight. It starts with one intentional decision, made with clear eyes about both the principles involved and the practical options available.

Sources:

¹ CNBC Select (2026), Interest rates for bank accounts are rising - here’s how you can take advantage. https://www.cnbc.com/select/bank-account-interest-rates-are-rising-how-you-can-take-advantage-/

² NerdWallet (2026), Average Bank Interest Rates for Savings Accounts, CDs and More. https://www.nerdwallet.com/banking/learn/average-rates-for-deposit-accounts

³ The Wall Street Journal Buy Side (2026), Today’s High-Yield Savings Rates: Up to 5.00%. https://www.wsj.com/buyside/personal-finance/banking/high-yield-savings-rates-today-5-6-2026

⁴ Financial Tech Lab (2025), How FDIC Insurance Really Works for Your Business Bank Account. https://www.youtube.com/watch?v=q8wVwGselzI&t=213s

Disclaimer:

This material is strictly for illustrative, educational or informational purposes only and does not constitute financial, investment, or legal advice. This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. Investing involves risks, including the loss of principal. Past performance does not guarantee future results. We recommend consulting a qualified Islamic scholar for guidance on your specific situation. Past performance is not indicative of future results. Wahed Invest LLC is a registered investment adviser with the SEC.

Certain content represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results; material is as of the dates noted and is subject to change without notice. The term halal denotes that permissibility in accordance with Islamic law.