Key Takeaways:

You have $50,000 in a savings account earmarked for serious long term investing, and the question is whether to point it toward a property down payment or toward a halal stock portfolio. Both pathways can help build real wealth in the U.S. Both come with sharply different demands on capital, risk, liquidity, time, and Shariah compliance. The honest answer is rarely "one is better." It is usually "which one fits the job this money needs to do?"

This article compares real estate vs stock market investing through what matters most for Muslim investors: return drivers, risk, time, capital, liquidity, and halal considerations. The goal of any property vs stocks investment debate is not to crown a winner but to give a framework for halal investing real estate vs stocks decisions.

Why This Comparison Matters

Real estate and stocks are the two most common wealth building pathways for U.S. households. The U.S. Census Bureau¹ put the first quarter 2026 homeownership rate at 65.3 percent, statistically similar to 65.7 percent in the fourth quarter of 2025. Stocks are not far behind: the Federal Reserve's Survey of Consumer Finances² reported 58 percent of U.S. families owned stocks (direct and indirect combined).

The barriers look different. The National Association of REALTORS' 2025 Profile of Home Buyers and Sellers³ reported first time buyers fell to 21 percent of buyers, a historic low, with the median age of first time buyers rising to 40. Stock investing has grown more accessible through ETFs and managed portfolios, while down payments and prices have pushed property out of reach for younger buyers.

For Muslim investors, the comparison also runs through Shariah compliant investing principles: how the property is financed, who the tenants are, what the stocks hold, and whether interest is embedded.

Real Estate Investing Overview

Real estate investing means buying residential or commercial property for rental income, property appreciation, or both. This can be in the form of direct ownership, partnerships, funds, crowdfunding, and Real Estate Investment Trusts (REITs).

Direct ownership offers tangible asset exposure and an income stream when occupied, but requires capital, due diligence, financing, maintenance, tenant management, insurance, taxes, and liquidity planning.

Passive options for access to real estate asset class (partnerships, funds, crowdfunding, REITs) reduce the management burden but are not automatically halal. Each needs review of debt levels, income source, ownership rights, tenant activity, and Shariah oversight.

Stock Market Investing Overview

Stock market investing means buying ownership in companies, directly through stocks or indirectly through ETFs, mutual funds, and managed portfolios. Returns come from business growth, share price appreciation, and dividends. Two advantages over real estate stand out: lower starting capital and higher liquidity. Most stocks can be sold during market hours, with cash settling within days. ETFs and managed portfolios make portfolio diversification easier across companies and sectors.

Not every stock or ETF is halal. Halal stock investing requires two layers of screening: business activity (alcohol, gambling, tobacco, weapons, adult entertainment, conventional finance, and similar industries) and financial ratios (interest bearing debt and interest income). Conventional index funds and target date funds typically hold conventional banks, interest based securities, and other non compliant positions. See our guide to halal investing in the U.S. and our piece on what makes an ETF halal.

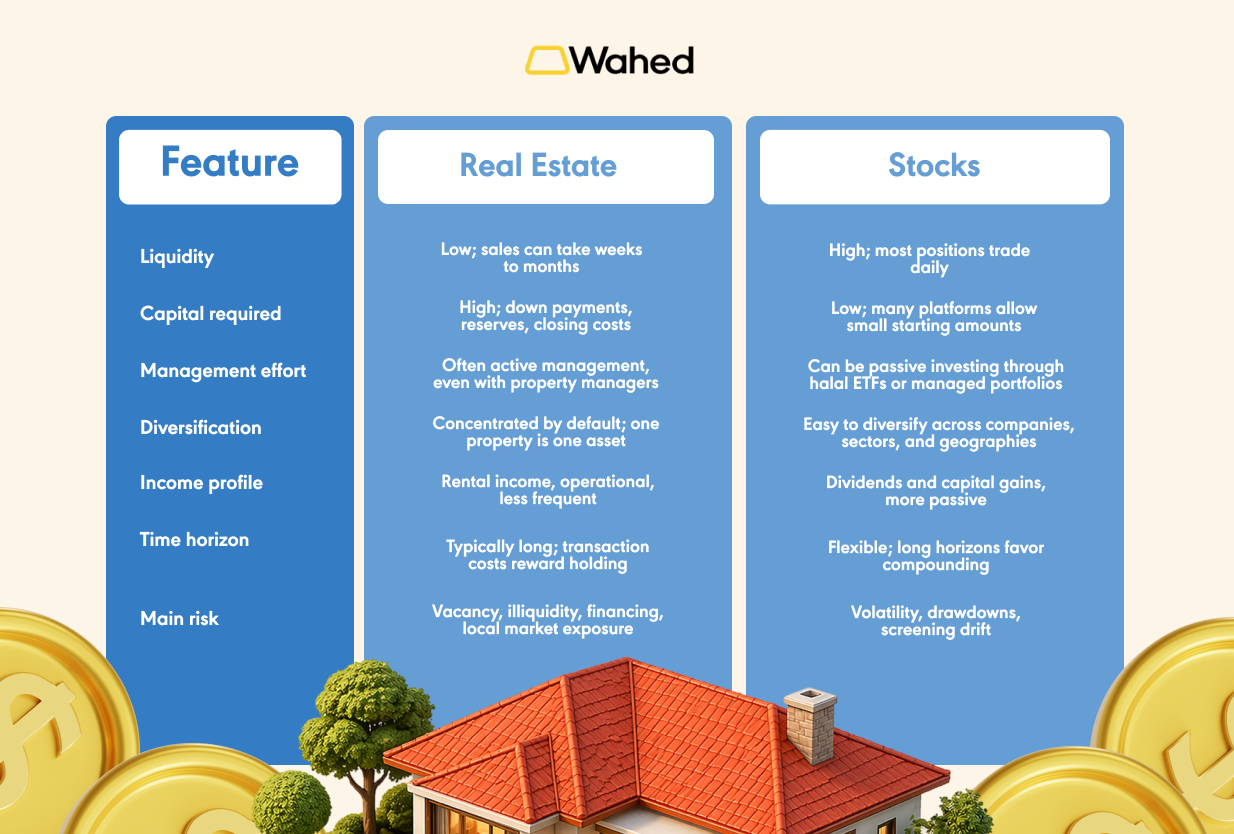

Key Differences Between Real Estate and Stocks

Side by side, the two asset classes serve different roles in a Shariah compliant portfolio.

Real estate concentrates capital into fewer assets, often with more control and more operational complexity. Stocks allow broader diversification and easier access, but they bring daily price volatility and require ongoing Shariah screening.

Returns from Real Estate vs Stocks

Real estate returns come from rental income and appreciation. Stock returns come from earnings growth, valuation expansion, dividends, and reinvestment. Both can compound over decades; both can also produce flat or negative outcomes over shorter windows. Real estate feels more stable because prices are not quoted every second, but values still rise and fall. Stocks feel more volatile because prices update daily, but diversified equity portfolios have historically been a major long term wealth building tool in the U.S.

Beating a diversified index is hard. The S&P Dow Jones Indices SPIVA U.S. Scorecard Year End 2024⁴ reported that 65% of active large cap U.S. equity funds underperformed the S&P 500 in 2024, with underperformance rising over longer horizons. A diversified, screened halal portfolio is often more disciplined than a handful of individually picked stocks. The better long term result is determined by structure, price paid, fees, time horizon, and discipline.

Risk Comparison

Both asset classes involve real risk. The risks show up differently.

Real Estate Risks

Illiquidity comes first: a property cannot be sold the way a stock can. Operational risk follows: damage, vacancy, maintenance, capital expenditures, and tenant turnover. Local market risk matters too; one neighborhood can underperform regional trends for years. Concentration risk matters: if most of an investor's net worth sits in one property, the portfolio is exposed to a single asset.

Stock Market Risks

Stock market risk is more visible because prices move daily. Volatility and drawdowns can be psychologically punishing, and behavioral mistakes (panic selling near the bottom, chasing winners near the top) can do as much damage as the market itself. Halal portfolios often tilt toward technology and healthcare after screening, which adds sector concentration risk. Holding non compliant companies by mistake, overlapping ETFs, and screening drift are quieter risks that compound. Fees and taxes matter over decades.

Time and Effort Required

Direct real estate is rarely truly passive. Even with a property manager, the owner handles property selection, major repairs, tax filings, insurance, and the bigger calls about whether to hold, refinance, or sell. Funds and platforms reduce that burden but introduce a different kind of work: evaluating each opportunity's structure, fees, leverage, and Shariah compliance. Stocks can be active or passive. Picking individual companies is real work, especially with ongoing Shariah screening. Halal ETFs and managed halal portfolios shift that work to the fund or advisor, which is why many busy professionals end up there. DIY gives maximum control but requires ongoing screening, allocation, rebalancing, and discipline; Shariah compliance is not a one time label, it is an ongoing process.

Example: Investing $50,000 in Real Estate vs Stocks

Imagine a 35 year old Muslim professional with $50,000 to invest for long term goals.

In the real estate path, the $50,000 might be a down payment, closing costs, and reserves on a rental property, or capital in a partnership. Direct ownership could generate rental income and property appreciation, but the investor likely needs additional cash for reserves and has to manage the property, vet tenants, and live with illiquidity.

In the stock portfolio path, the same $50,000 could go into a diversified halal stock portfolio, halal ETFs, or a managed halal portfolio matched to risk tolerance. The benefits are liquidity and diversification with less operational work; the trade off is daily volatility and ongoing Shariah compliance.

A balanced path also exists: keep a cash reserve, allocate part of the $50,000 to a diversified halal portfolio, and consider real estate later when capital, time horizon, and Shariah compliant structure align.

When Real Estate May Be Better

Real estate tends to fit when several things line up: enough capital, ability to handle illiquidity, desire for asset backed income, and willingness to evaluate property level risk. It also suits investors who want exposure different from public equities, can tolerate tenant and maintenance risk, and plan to hold long term. Rental income is a real return stream, but direct ownership almost always requires active oversight.

When Stocks May Be Better

Stocks tend to fit when the investor has less starting capital, wants liquidity, values easier diversification, and prefers a more passive path. They suit investors who want automated contributions through retirement accounts, do not want to manage tenants or repairs, and are building toward long term retirement. The investor needs to tolerate volatility and stay invested when prices fall. Halal ETFs and managed portfolios make stock market investing more accessible when the screening methodology is credible.

Should Muslim Investors Choose One or Both?

For many investors, it depends as each plays a different role. Stocks provide liquidity, growth exposure, and easier diversification; real estate provides tangible asset exposure, rental income, and a return profile different from public markets. The hard part is not owning both, but owning both at the right allocation, with the right structure, and with enough liquidity.

Our halal portfolio diversification strategy piece walks through allocation principles, and our piece on how to diversify into real estate without buying property covers funds, REIT screening, and indirect paths. For busy Muslim professionals, a managed halal portfolio can be the structured foundation, with real estate added when the investor understands the liquidity, capital, and Shariah requirements of a specific deal.

Common Mistakes Muslim Investors Make When Comparing Real Estate and Stocks

- Assuming REITs are automatically halal. Many carry interest bearing debt or non compliant tenants.

- Treating rental income as fully passive. Direct ownership creates real work even with a manager.

- Concentrating too much in one property. A single asset can dominate portfolio risk.

- Avoiding stocks because of short term volatility. Diversified, screened equity portfolios have historically built long term wealth.

- Buying mainstream ETFs without checking holdings. Standard index funds often include non compliant exposure.

- Comparing returns without netting fees, repairs, financing, insurance, and taxes. The picture changes.

- Holding too much cash while waiting for the "perfect" property. Idle cash erodes purchasing power.

- Choosing based on social media hype. Match the asset to goals, time horizon, and Shariah requirements.

Build a Balanced Halal Investment Strategy

The decision should not be driven by hype, family pressure, or fear of missing out. It should be driven by goals, time horizon, liquidity needs, Shariah compliance, and the operational effort the investor wants to manage. Real estate may suit investors with capital, patience, and the ability to handle illiquidity; stocks may suit those who value liquidity, diversification, and a passive path. For most Muslim investors, the strongest answer is a deliberate combination rather than an either/or choice.

Sources:

¹ U.S. Census Bureau, Quarterly Residential Vacancies and Homeownership, First Quarter 2026. https://www.census.gov/housing/hvs/current/

² Federal Reserve, Changes in U.S. Family Finances from 2019 to 2022: Evidence from the Survey of Consumer Finances. https://www.federalreserve.gov/publications/october-2023-changes-in-us-family-finances-from-2019-to-2022.htm

³ National Association of REALTORS, 2025 Profile of Home Buyers and Sellers, Highlights. https://www.nar.realtor/sites/default/files/2025-11/2025-profile-of-home-buyers-and-sellers-highlights-11-04-2025.pdf

⁴ S&P Dow Jones Indices, SPIVA U.S. Scorecard Year-End 2024. https://www.spglobal.com/spdji/en/documents/spiva/spiva-us-year-end-2024.pdf

Disclaimer:

Risk Disclosure: For U.S. audience. Wahed Invest LLC (Wahed) is a U.S. Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only. Diversification does not guarantee a profit or protect against loss. Risk/reward profile of any asset class can vary significantly.