UK Autumn Budget 2024: Major IHT changes for UK Businesses

Autumn Budget 2024: Inheritance Tax Hike on UK Business Owners

Ruzwan Boota (Tax Director at I Will Solicitors Limited) delves deeper into a significant announcement in the Autumn Budget on 30 October that completely changes the status quo for business owners in the UK, and will likely drag many of them into having a significant exposure to Inheritance Tax (IHT) should they pass away after 6 April 2026.

(I Will Solicitors Ltd is a wholly owned subsidiary of Wahed Inc. They provide Islamic Wills, Probate and Tax Advisory services).

After reflecting on the announcements in the Autumn Budget and trawling through the details in the policy documents, there is one announcement which I am worried will go unnoticed by many business owners, but could likely impact them and their families more than any other - and that is the change to IHT Business Relief.

The Chancellor announced that, effective from 6 April 2026, Business Relief will only be available at a rate of 100% on the first £1m of qualifying assets (e.g. shares in a trading business) and it will be restricted to 50% thereafter.

On the face of it, it may not seem like a big change, but below is an example which sheds light on just how significant the impact could be.

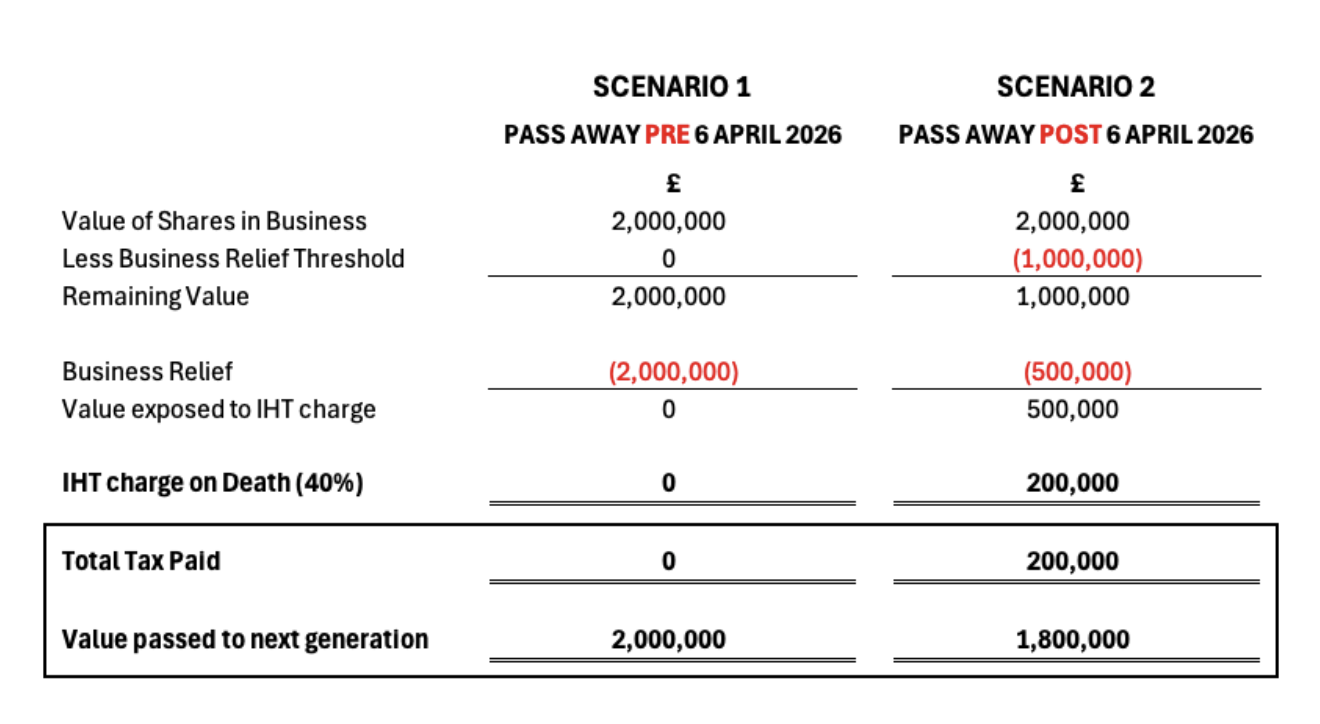

Let’s say that Mr Khan is the sole shareholder of his wholesale business which is worth £2m.

Historically, any qualifying business (essentially most trading businesses) would benefit from 100% Business Relief on death, therefore Mr Khan would not have to worry about IHT on the value of the shares in his business (regardless of its value), and his shares would then pass to his inheritors with no tax charge, and therefore no tax problem.

However under the new provisions, if Mr Khan passes away post 6 April 2026, his shares in the business would be exposed to a £200,000 IHT charge - big problem!

Here is a breakdown of the calculation:

Now whilst the amount of tax is already a blow to the inheritors, the pressing question is - how will the inheritors pay for it?!

Unless there is already significant cash within the estate to pay the IHT liability, they will essentially have four options:

1. Sell (in whole or part) the shares in the business

If they sold the shares pre-death, there are likely to be significant tax charges (Capital Gains Tax (CGT) and IHT). In the above case for Mr Khan, the overall tax liability could be up to c.£1.09m, meaning an overall effective tax rate of c.54% on death! This would leave the inheritors with only c.£910k to split between them from the original £2m!

If they sold the shares immediately post-death, under the current provisions, there will likely be no CGT as there will be a tax-free uplift in the base cost of the shares post-death. Therefore the only tax liability will be the IHT liability of £200,000. This would leave the inheritors with £1.8m to split between them.

2. Keep the business and use profits to pay the IHT liability

If the inheritors decide to continue operating the business and use company profits to pay the IHT liability, the tax implications increase significantly. Based on a company value of £2m, the total tax liabilities would be c.£440k (combination of IHT, Income Tax on dividend and Corporation Tax on profits). That means incurring a further £220k of tax in order to pay a £200k tax liability!

Note too that if you are paying the IHT in instalments over a period of time, you will also need to factor in that HMRC have increased the interest rate on unpaid tax liabilities by 1.5 percentage points to Bank Rate plus 4 percentage points (currently the interest rate on IHT liabilities is 7.5%, so it will jump up further to 9%!).

3. Sell other assets to fund the liability

If there are other assets in the estate (e.g. home, rental properties, etc), the inheritors could choose to sell those assets and use the net sale proceeds (after further tax potentially) to settle the IHT liability.

This could cause potential issues for the inheritors, and is not at all practical if the only other asset is the home which the surviving spouse is continuing to live in.

4. The inheritors take out a loan to pay the liability

Unless there is an asset (e.g. property) to take out the loan against, this will likely result in the inheritors taking out a conventional loan rather than a Shariah Compliant Loan and therefore getting into Riba (interest), which opens another can of worms! #WithdrawFromRiba

(Note that the effective tax rates mentioned above can change with the value of the business. If the value of the shares in the business is greater than the one used in the example, the effective tax rate will be higher).

Significant impact for business owners

The above represents a significant change for business owners and their families, particularly those with a business worth over £1m. What many people have done for such a long time here in the UK is build family businesses that grow over time and then let it pass to the next generation tax free. This will likely change now as a result of these announcements.

Why is the Government doing this? It seems that instead of letting people pass on businesses tax free to inheritors (and as a result, wait potentially a few generations before any CGT & IHT receipts on the value), they are pushing for the CGT and IHT receipts to arrive sooner into the Treasury, alongside higher dividend tax, corporation tax and interest receipts if the inheritors keep the business and pay the IHT liability over time.

There is a real lack of knowledge about IHT, and in some cases a real lack of action as people bury their heads in the sand hoping that the problem will go away. These changes announced in the Autumn Budget will only cause more problems for people going forward so it is vital (more than ever before) that business owners seek advice on IHT and their potential exposure and plan for succession so that it all doesn’t come as a surprise to family members after the death of a loved one.

There are actions that can be taken to manage this impact, but they must be planned well in advance in order to get maximum benefit.

Want to discuss what actions you can take to navigate the changes?

If you would like to discuss planning opportunities in the wake of the Budget, we are offering free 30 minute meetings with Ruzwan Boota and Wahed’s Head of Private Clients Services UK, Abul Fazal Salahuddin. If you would like to book in a meeting, please do so using the following link:

Risk Warning: Equity investments are not readily realisable and involve risks, including loss of capital, illiquidity, lack of dividends and dilution, and it should be done only as part of a diversified portfolio. Investments of this type are only for investors who understand these risks. You will only be able to invest in the company once you have met our conditions for becoming a registered member.

Please visit www.wahed.com/uk/ventures/risk for our full risk warning.

Risk Warning: As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Please visit www.wahed.com for our full terms and conditions

Maydan Capital Limited, trading as WahedX, is registered in England and Wales (Company No. 13451691), registered office: 87-89 Baker Street, London, W1U 6RJ, UK. Maydan Capital Ltd (FRN: 963613) is an appointed representative of Wahed Invest Ltd (FRN: 833225), an authorised and regulated firm by the Financial Conduct Authority.Wahed Invest Ltd. is registered in England and Wales (Company No. 10829012), registered office: 87-89 Baker Street, London, W1U 6RJ, UK and is authorised and regulated by the Financial Conduct Authority: FRN 833225.

Subscribe For More Islamic Finance Content

As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Wahed Invest LLC (Wahed) is a US Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.

Disclaimer: Wahed Technologies Sdn Bhd ("Wahed") is a Digital Investment Manager (DIM) licensee issued by Securities Commission Malaysia (eCMSL/ A0359/2019). It is part of Wahed Inc. Wahed is authorized to conduct a fund management business that incorporates innovative technologies into automated portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007. All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The history of returns, expected returns, and probability projections is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for liability for your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system, and do not indicate future returns that will be realized by you.

Wahed Limited - Nigeria: All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The historical returns and expected returns is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for any losses arising from your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system and do not indicate future returns that will be realized by you. Wahed Limited (Wahed) is registered and regulated by the Securities and Exchange Commission, Nigeria. Wahed Limited is a subsidiary of Wahed Inc. Please visit www.wahed.com for full terms and conditions.

Wahed Invest Limited is regulated by ADGM’s Financial Services Regulatory Authority (“FSRA”) as an Islamic Financial Business with Financial Services Permission for Shari’a Compliant Regulated Activities of Managing Assets and Arranging Custody [Financial Permission No. 220065]. Our ADGM Registered No. is 000004971.

Wahed assumes no obligation to provide notifications of changes in any factors that could affect the information provided. This information should not be relied upon by the reader as research or investment advice regarding any issuer or security in particular. Any strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. Furthermore, the information presented may not take into consideration commissions, tax implications, or other transactional costs, which may significantly affect the economic consequences of a given strategy or investment decision. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance.

There is no guarantee that any investment strategy will work under all market conditions or is suitable for all investors. Each investor should evaluate their ability to invest long term, especially during periods of downturn in the market. Investors should not substitute these materials for professional services and should seek advice from an independent advisor before acting on any information presented. Any links to third-party websites are provided strictly as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites. When you access one of these websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites.