Choosing the Right Portfolio: A Guide to Getting Started

If you're new to the concept of portfolios, the term might feel a bit abstract. Perhaps you're more familiar with individual stocks or funds, and suddenly you're faced with choosing between "Very Conservative" and "Very Aggressive" options. It's natural to feel uncertain.

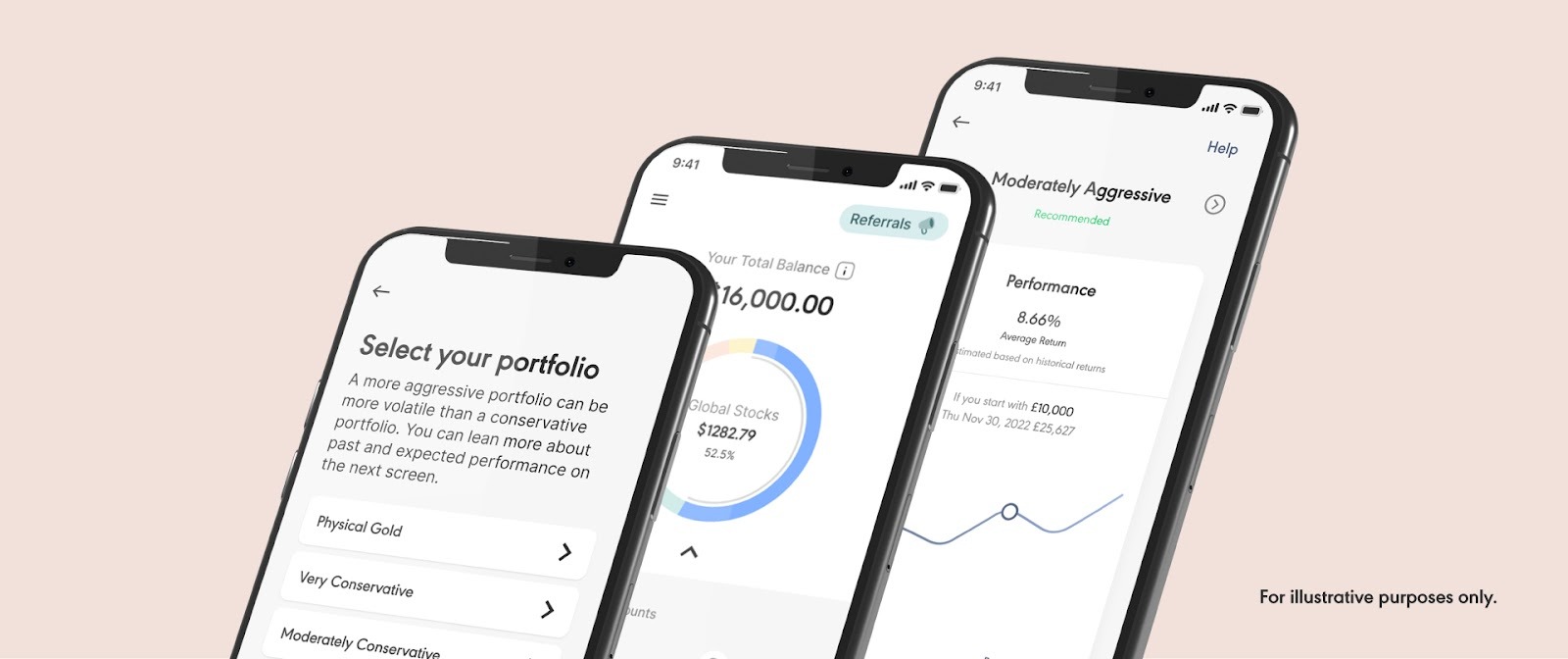

At its core, a portfolio is simply a collection of different investments working together. Each portfolio at Wahed combines different asset classes in specific proportions, designed to achieve different goals whilst remaining entirely shariah-compliant.

Before we explore how these portfolios differ and which might suit your circumstances, let's look at what they all have in common.

What Every Wahed Portfolio Shares

Managed Portfolios

Investments require ongoing attention, even when they're held within funds that have their own managers. The team at Wahed actively manages the proportions invested across the funds that make up each portfolio. This means monitoring market conditions, adjusting weightings when needed, and working to improve returns whilst managing risk. It's not a set-and-forget approach for us.

Active management means our clients don’t have to watch market movements or make complex allocation decisions themselves. It’s handled by professionals who oversee portfolios.

Shariah Compliance

For many people exploring halal investing, knowing that investments align with their faith provides genuine peace of mind. Every investment within Wahed's portfolios undergoes rigorous shariah compliance screening, both by internal teams and external auditors.

What does this screening actually involve? It operates on two levels:

Business Activity Screening examines what a company actually does. This excludes companies involved in activities prohibited under Shariah: tobacco, alcohol, gambling, conventional interest-based institutions, weapons manufacturing, adult entertainment, and impermissible food products. The focus here is ensuring the core business itself is permissible.

Financial Ratio Screening looks at how a company manages its finances. Even if a company's primary business is halal, Shariah guidelines set boundaries around debt levels, the proportion of income from impermissible sources, and cash holdings. These ratios ensure that a company's financial structure remains within acceptable limits.

Should any impermissible gains inadvertently occur (sometimes unavoidable in complex corporate structures), Wahed provides a purification report. This allows investors to offset these gains, maintaining the purity of their returns.

Understanding the Differences Between Portfolios

Now to what makes each portfolio distinct.

Every portfolio differs in three fundamental ways:

- The asset classes it invests in

- How much gets allocated to each asset class

- How investment is distributed amongst funds within those asset classes

In simpler terms, whilst portfolios might contain similar types of investments, the proportions vary considerably. One portfolio might lean heavily into stocks, another might favour sukuk, whilst others strike a balance. These different compositions aren't arbitrary; they're designed to reflect different levels of risk and potential return.

The Risk Spectrum

Risk in investing isn't about recklessness or caution in the everyday sense. It's about volatility, the degree to which an investment's value might fluctuate over time.

Stocks, by their nature, tend to be more volatile. Their values can rise and fall more dramatically in response to market conditions, company performance, and broader economic factors. This volatility brings potential for higher returns, but also the reality of sharper downturns.

Sukuk, on the other hand, are typically lower risk. They represent ownership in tangible assets or services, providing more stable, predictable returns. The trade-off is that this stability usually means lower growth potential.

Gold sits somewhere distinct, often serving as a hedge against economic uncertainty whilst offering different characteristics to both stocks and sukuk.

With this understanding, the portfolio names begin to make sense. Here's how they're structured:

Very Conservative – 99% sukuk, 1% cash

Focuses on capital preservation with minimal volatility.

Moderately Conservative – 65% sukuk, 33% stocks, 4% gold, 1% cash

Allows for gradual growth whilst prioritising stability.

Moderate – 50% sukuk, 42.25% stocks, 6.75% gold, 1% cash

A balanced approach blending stability with growth potential.

Moderately Aggressive – 55.25% stocks, 35% sukuk, 8.75% gold, 1% cash

Growth-oriented whilst maintaining some stability.

Aggressive – 77.5% stocks, 15% sukuk, 6.5% gold, 1% cash

Focused on long-term wealth accumulation.

Very Aggressive – 99% stocks, 1% cash

Maximum equity exposure for those seeking highest growth potential.

Gold Portfolio – 100% physical gold exposure through The Royal Mint Physical Gold ETC

A specialist option for those seeking gold's unique characteristics as an asset class.

The pattern is clear: as stock allocation increases, so does potential return and volatility. As sukuk allocation increases, stability improves but growth potential typically moderates.

Detailed breakdowns of each portfolio's holdings are available on their individual pages for those wanting to understand the specifics.

Choosing What Fits Your Circumstances

Here's where things get personal, and where we need to be clear: everyone's situation is unique. Nothing here constitutes financial advice for your specific circumstances. If you need tailored guidance, seeking advice from a qualified financial adviser is important.

What we can offer is a framework for thinking through the considerations that matter when assessing suitability.

Your Goals Shape Everything

Investment decisions rarely exist in isolation. They're usually connected to something meaningful, whether that’s building financial security, working towards a milestone, or simply ensuring money retains its value over time.

When thinking about goals, three considerations tend to emerge:

Time horizon - How long before funds might need to be accessed?

Liquidity requirements - Will money need to be withdrawn along the way, or can it remain invested?

Target outcomes - What are the aims? Capital preservation? Growth? Both?

Getting clarity on these can help narrow down which portfolios might align with particular circumstances.

Understanding Risk

There's an important distinction here that often gets overlooked.

Risk tolerance is emotional. It's about how comfortable someone feels watching their investment value fluctuate. Some people find significant volatility stressful, even if they can logically afford the risk. Others remain composed during market downturns. Neither response is wrong; they're just different temperaments.

Risk capacity is practical. It's about actual financial ability to withstand potential losses. Someone with decades until retirement and a stable income has different risk capacity than someone needing funds within two years.

Ideally, a chosen portfolio aligns with both tolerance and capacity. Investing in an aggressive portfolio when lacking emotional comfort with volatility can lead to poor decisions during market downturns. Equally, playing it too safe when having both the capacity and long time horizon might mean missing growth opportunities.

Time Horizons in Practice

Let's look at how different time horizons might influence portfolio considerations. Remember, these are illustrative examples to show a thinking process, not recommendations for specific situations.

Longer Time Horizons

Consider someone with 15 or more years before needing to access funds. Perhaps it's the beginning of retirement planning, or building a substantial fund for the distant future.

With many years ahead, there's opportunity to experience market cycles. Markets rise and fall; it's their nature. But over extended periods, they've historically trended upward. This longer runway potentially allows for taking on more volatility in exchange for growth potential.

Someone in this position might consider portfolios towards the aggressive end of the spectrum. The compounding effect over such a lengthy period can be meaningful, and there's time to recover from market downturns that inevitably occur.

Medium Time Horizons

Someone saving towards a goal five to ten years away faces different considerations. It might be contributing to a child's future education costs, building a deposit, or working towards a life milestone.

Here, there's still time to ride out some market volatility, but the end point is coming into view. This might suggest starting with moderately aggressive or aggressive options to capture growth, then gradually shifting towards more conservative portfolios as the time horizon shortens.

This phased approach aims to benefit from growth potential early on, then progressively prioritise capital preservation as the need for funds approaches. It's not about timing the market, but about adjusting risk exposure as circumstances change.

Shorter Time Horizons

Consider nearer-term liquidity needs, perhaps within one to three years. This might be building an emergency fund, saving for a wedding, or accumulating funds for a house purchase in the relatively near future.

With less time available, there's limited opportunity to recover from significant market downturns. If the market drops sharply just before funds are needed, there may not be time for recovery.

This scenario typically calls for managing volatility carefully. Portfolios ranging from Very Conservative to Moderate might be more suitable here. The focus shifts towards preservation and steady, modest growth rather than chasing higher returns. Even beating inflation whilst protecting capital can be a meaningful outcome over such periods.

The Gold Portfolio

Gold occupies a unique position in investment strategies. It doesn't generate income like sukuk or growth like equities, and it often behaves differently to other asset classes during various economic conditions.

During the 2008 financial crisis, for instance, global stocks fell sharply by 49%, whilst gold rose by 47%, demonstrating how it can move independently of traditional markets during periods of significant stress. This contrasting behavior is part of what makes gold an interesting diversification tool.

Some people allocate to gold as a hedge, a way of diversifying beyond traditional stocks and bonds. Others view it as a store of value during uncertain times. The Gold Portfolio offers 100% exposure for those who specifically want this metal as part of their overall investment approach.

It's worth noting that gold is already included across several portfolios, ranging from 4% in Moderately Conservative to 8.75% in Moderately Aggressive. The standalone Gold Portfolio exists for those wanting dedicated gold exposure beyond these allocations, perhaps as part of a broader multi-portfolio strategy.

Performance Considerations

Looking at historical performance, aggressive portfolios have typically outperformed moderate and conservative ones, which aligns with expectations given their higher risk profile. However, this observation requires context.

Past performance offers no guarantees about future results. Markets behave differently across various periods, and what worked historically may not repeat. Higher returns have historically come with higher volatility, meaning sharper declines during difficult market periods.

The "best performing" portfolio isn't necessarily the right portfolio. It depends entirely on individual circumstances, goals, and the ability to remain invested through market fluctuations.

Portfolio Transitions and Flexibility

Life isn't static, and neither should investment approaches be.

Perhaps someone started investing with a long time horizon and chose an aggressive portfolio. Several years later, their goals have evolved or their need for liquidity has shifted. The ability to transition between portfolios allows for adapting as circumstances change.

At Wahed, moving between portfolios is possible. As time passes and goals come closer to fruition, the option to dial down volatility and increase capital preservation can be valuable. Similarly, if risk capacity increases, moving towards more growth-oriented portfolios is feasible.

It's also worth knowing that having multiple portfolios simultaneously is possible. Different goals might warrant different approaches. Someone might maintain a Very Aggressive portfolio for long-term wealth building whilst also holding a Conservative portfolio for nearer-term needs. Each operates independently, allowing for tailored strategies across different objectives.

This flexibility means early portfolio choices aren't permanent commitments. They're starting points that can evolve alongside changing circumstances.

Making Your Choice

Choosing a portfolio isn't about finding the objectively "best" option, because no such thing exists. It's about finding what aligns with specific circumstances, goals, and comfort levels.

The framework for thinking this through involves:

- Clarifying time horizons and liquidity needs

- Understanding both emotional tolerance for volatility and practical capacity for risk

- Recognising that circumstances change, and portfolios can adapt accordingly

- Remembering that different goals might warrant different approaches

As understanding deepens and comfort grows, adjustments can always be made. The important thing is starting with something that feels manageable and aligns with current circumstances.

Every journey begins somewhere. The portfolios exist to serve different needs, different timelines, and different approaches to balancing growth with stability. Understanding what sits behind each option is the first step towards making an informed choice.

Risk Warning: Equity investments are not readily realisable and involve risks, including loss of capital, illiquidity, lack of dividends and dilution, and it should be done only as part of a diversified portfolio. Investments of this type are only for investors who understand these risks. You will only be able to invest in the company once you have met our conditions for becoming a registered member.

Please visit www.wahed.com/uk/ventures/risk for our full risk warning.

Risk Warning: As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Please visit www.wahed.com for our full terms and conditions

Maydan Capital Limited, trading as WahedX, is registered in England and Wales (Company No. 13451691), registered office: 87-89 Baker Street, London, W1U 6RJ, UK. Maydan Capital Ltd (FRN: 963613) is an appointed representative of Wahed Invest Ltd (FRN: 833225), an authorised and regulated firm by the Financial Conduct Authority.Wahed Invest Ltd. is registered in England and Wales (Company No. 10829012), registered office: 87-89 Baker Street, London, W1U 6RJ, UK and is authorised and regulated by the Financial Conduct Authority: FRN 833225.

Subscribe For More Islamic Finance Content

As with any investment, a Wahed Invest Ltd investment puts your money at risk, as the value of your investment can go down as well as up. The tax treatment of your investment will depend on your individual circumstances and may change in the future. If you are unsure about whether investing is right for you, please seek expert financial advice.

Wahed Invest LLC (Wahed) is a US Securities and Exchange Commission (SEC) registered investment advisor. Wahed Invest provides brokerage services to its clients through its brokerage partner Apex Clearing Corporation, a member of NYSE - FINRA - SIPC and regulated by the SEC and the Commodity Futures Trading Commission. Registration does not imply a certain level of skill or training. Wahed does not intend to offer or solicit anyone to buy or sell securities in jurisdictions where Wahed is not registered or a region where an investment practice like this would be contrary to the laws or regulations. Any returns generated in the past do not guarantee future returns. All securities involve some risk and may result in loss. Any performance displayed in the advertisements or graphics on this site are for illustrative performances only.

Disclaimer: Wahed Technologies Sdn Bhd ("Wahed") is a Digital Investment Manager (DIM) licensee issued by Securities Commission Malaysia (eCMSL/ A0359/2019). It is part of Wahed Inc. Wahed is authorized to conduct a fund management business that incorporates innovative technologies into automated portfolio management services offered to clients under a license issued pursuant to Schedule 2 of the Capital Markets Services Act 2007. All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The history of returns, expected returns, and probability projections is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for liability for your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system, and do not indicate future returns that will be realized by you.

Wahed Limited - Nigeria: All investments involve risks, including the possibility of losing the money you invest, and the track record does not guarantee future performance. The historical returns and expected returns is provided for informational and illustrative purposes, and may not reflect actual future performance. Wahed is not responsible for any losses arising from your trading and investment decisions. It should not be assumed that the methods, techniques, or indicators presented in this product will be profitable, or will not result in losses. The previous results of any trading system published by Wahed, through the Website or otherwise, do not indicate future returns by that system and do not indicate future returns that will be realized by you. Wahed Limited (Wahed) is registered and regulated by the Securities and Exchange Commission, Nigeria. Wahed Limited is a subsidiary of Wahed Inc. Please visit www.wahed.com for full terms and conditions.

Wahed Invest Limited is regulated by ADGM’s Financial Services Regulatory Authority (“FSRA”) as an Islamic Financial Business with Financial Services Permission for Shari’a Compliant Regulated Activities of Managing Assets and Arranging Custody [Financial Permission No. 220065]. Our ADGM Registered No. is 000004971.

Wahed assumes no obligation to provide notifications of changes in any factors that could affect the information provided. This information should not be relied upon by the reader as research or investment advice regarding any issuer or security in particular. Any strategies discussed are strictly for illustrative and educational purposes and should not be construed as a recommendation to purchase or sell, or an offer to sell or a solicitation of an offer to buy any security. Furthermore, the information presented may not take into consideration commissions, tax implications, or other transactional costs, which may significantly affect the economic consequences of a given strategy or investment decision. This information is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance.

There is no guarantee that any investment strategy will work under all market conditions or is suitable for all investors. Each investor should evaluate their ability to invest long term, especially during periods of downturn in the market. Investors should not substitute these materials for professional services and should seek advice from an independent advisor before acting on any information presented. Any links to third-party websites are provided strictly as a courtesy. We make no representation as to the completeness or accuracy of information provided at these websites nor do we endorse the content and information contained on those sites. When you access one of these websites, you are leaving our website and assume total responsibility and risk for your use of the third-party websites.